- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- Where have all of the Syndicate Leads Gone?

Where have all of the Syndicate Leads Gone?

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

July 17, 2024

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

Fill out our unique form to get to the top of the line here.

Deal Sheet = Access the Best (weekly) SPV Investment Opportunities @ Discounted Carry

To get access to these deals at 10% carry you can sign up for Deal Sheet here or book a call to learn more!

Where have all the syndicate leads gone?

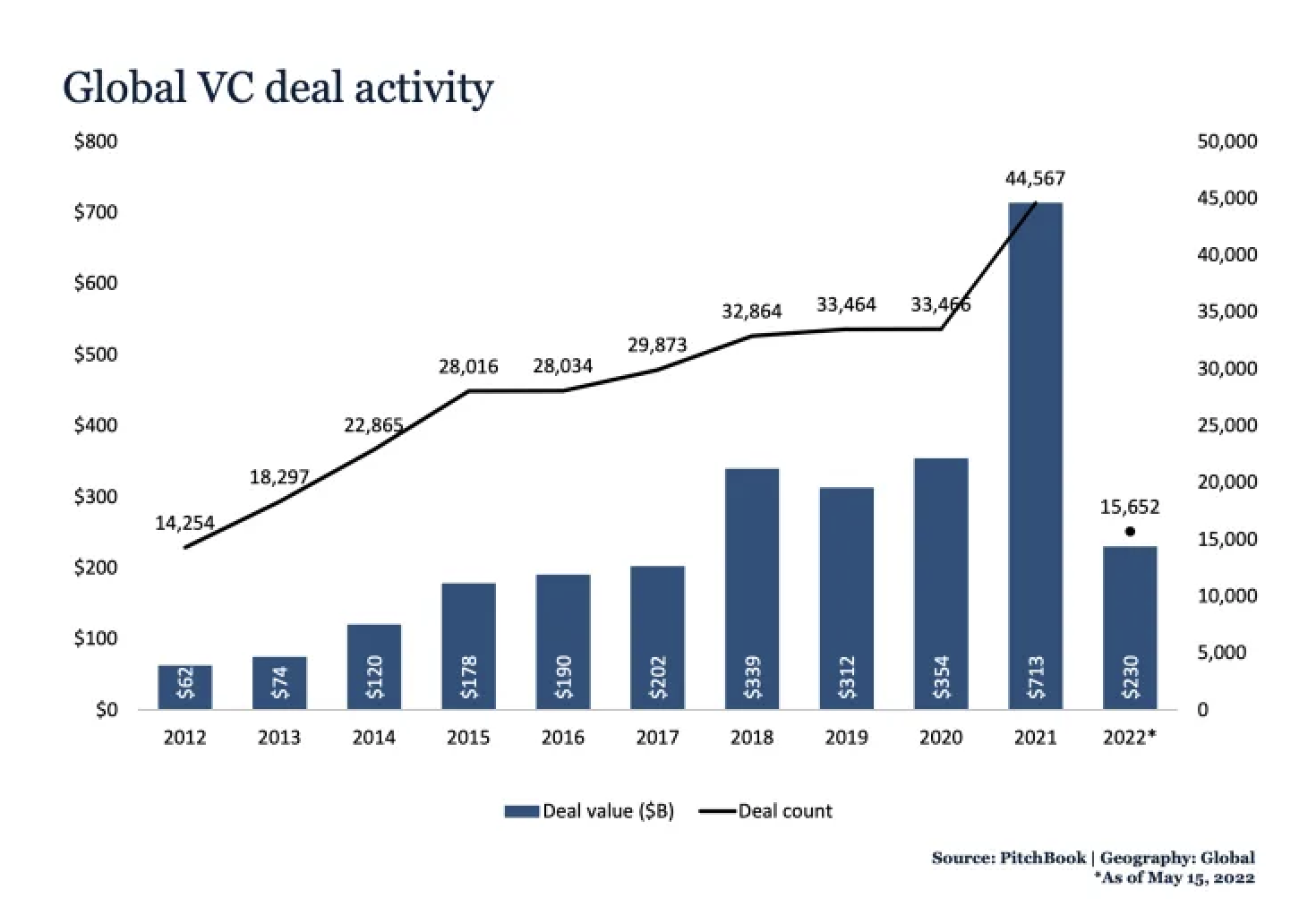

The past 5 years have been rocky in venture capital. Through the hype cycles and downturns, we witnessed a massive growth in SPV managers and then a sharp drop off. This is very much correlated to the macro environment in VC.

It feels like many of the syndicate leads that were around in our SPV early days (2019-2021) have since dropped off from venture or have gone on to pursue other initiatives within VC. Even just 4-5 years ago the VC world felt much different than it currently does as we’ve seen so much change in markets and a global pandemic making the venture capital ecosystem quite chaotic.

When we started getting active in running syndicates back around 2019, Venture Capital felt buzzier. It felt like just about all accredited investors were interested on some level to get involved in the asset class and try to invest in the next Uber, Airbnb and so on. The emergence of syndicates at the time was likely the best avenue for many of these accredited individual investors to access the venture capital asset class via deals led by syndicate leads. It was an exciting time to be a syndicate lead and frankly an easier time to put capital to work given the volume of capital flowing into the VC ecosystem.

Fast forward just 5 short years to the present day where, in that time, many twists and turns occurred in the world and very much in Venture Capital. Valuations have come down (in most industries), IPOs are slow and few, large tech M&A events are much fewer, and it’s generally much harder for founders to raise capital (especially growth capital) as VC’s are evaluating companies differently than just a few years ago. There was previously a period in 2021, where margins, capital efficiency and overall business model sustainability was heavily discounted against top line growth as one example - that has all changed.

In this post, we are going to explain our take on:

The drop off in active syndicate leads

Where did the syndicate leads move on to

General thoughts on what it suggests about the syndicate leads who are still around and active

Where did they all go?

2022 Market Correction

After the post-covid ZIRP era when capital was flowing unlike anything we’d seen previously, VC started to take a sharp turn in Q1/Q2 2022. This was undoubtedly felt by all syndicate leads similar to the way it was felt by VC’s. In Q1 2022, fewer startups were getting funded and lots of VCs shifted focus to their existing portfolio companies to navigate reducing burn and extending runway for unknown times ahead. The funding environment quickly became terrible and few companies wanted to be in a position to need to raise new capital during this time and/orbe forced to do a down round (and massively dilute themselves and investors). So, the general mentality was do what you need to not rely on raising additional outside capital for the near future or receive bridge financing support from existing cap table investors.

There are few companies that exemplify this period than Bird, the scooter company that went public at an implied $2.3B (approx) valuation, and has since been delisted from the New York Stock Exchange because of its inability to lift its market cap to $15 million. Bird unfortunately is emblematic of a large swath of growth stage companies that were overvalued and VCs and founders immediately took note.

With this VC/founder mentality, it meant:

a sharp decline in new companies getting funded.

longer diligence processes and slower deployment periods

general hesitation to deploy capital into new companies (especially growth companies) for an extended period

This translated to the syndicate ecosystem as well. As syndicate leads, we are primarily investing alongside traditional VC’s and not leading rounds. With the number of VC funded rounds occurring shrinking, as did VC syndicate deal flow.

This goes to show:

How reliant syndicates are on VC’s doing deals and leading funding rounds and

How cyclical this ecosystem has been over the years (read our previous post, specifically the third point on cyclicality in our article “5 VC Syndicate Learnings After Closing 500 SPVs”)

In addition to the very low deal volume, the LP community turned pretty bearish and cynical on venture (and understandably). Many companies were heavily reliant on more capital. There were tons of down rounds, mark downs, companies going out of business (or months away from bankruptcy) and therefore a newly adjusted (extended) timeline to liquidity and positive outcomes for existing portfolio companies.

The enthusiasm of syndicate leads in securing allocations for promising deals was met with tepid response from limited partners (LPs), resulting in minimal capital flow to support special purpose vehicles (SPVs). This shift in investor sentiment quickly became apparent, significantly hampering syndicate leads' ability to deploy capital through the SPV model and potentially earn future carried interest. This trend was evident across one of the major fund admin platforms, prompting the fund admin to temporarily relax its rules and allowing for lower investment minimums, enabling syndicate leads to form SPVs without incurring out-of-pocket costs. This policy adjustment was a direct response to the sharp decline in LP interest and capital deployment, aimed at supporting general partners (GPs) in closing deals despite reduced funding levels.

My Main Takeaways:

It quickly became a way harder job being a syndicate lead in 2022 than anything we had experienced leading up to this. For that reason, many syndicate leads felt it was not worth it pulling teeth to try and get SPV’s done only to come up short in LP capital committed and decided to no longer syndicate deals and therefore left the syndicate ecosystem… and have not come back. 👋

The traditional venture capital ecosystem is seeing this now too, specifically for new emerging managers and emerging funds looking to raise a fund 2 or fund 3 whereas their previous fund is not performing well (for timing reasons explained above). Even the mega funds like Tiger and Insight had to reduce their fundraising targets massively. Similar to the individual accredited investor community, the larger institutional LP community is rethinking their deployment strategy into venture funds, likely making it tougher to raise capital (not a bad thing). The main difference is that fund cycles are way longer than syndicates, so while many syndicates have left the ecosystem, I think we’ll see the same of venture capital funds, however it will play out over 5 years, whereas one could say the syndicate drop off really happened within 1 year.

Leaving Syndicates to Start a Fund

It is my belief that many people start syndicates to go on and raise a traditional venture fund. Most folks want to raise capital from institutional/higher net worth LPs, have capital they can deploy at their discretion, and also be able to make a living and build a true VC firm with management fees (remember, syndicate management fees are either 0 or minimal). After all, this is how traditional venture capital works and what many, I would say most folks in venture, strive to do.

It should not come as a surprise that many syndicate leads start with the SPV ecosystem to build a track record and an LP-base to level-up to go on and raise a fund, where the GP can have full capital deployment discretion and take larger management fees.

Earlier in this post, I highlighted the market correction as the catalyst for syndicates leaving the ecosystem or in other words failing, whereas going on to raise a fund is quite the opposite. I view that more as a graduation from syndicates to a traditional venture capital fund. Most syndicates are likely unable to raise a fund, therefore, only the higher quality syndicates put in the work to position them to go on to raise a fund. Even though I've been excited to double/triple down on syndicates, I equally can understand the rationale to wanting to build a traditional venture fund, and institutionalize your firm.

As a reminder, we see many folks enter the syndicate ecosystem because it is a good place to establish yourself as a potential fund manager. Starting with SPVs allow for:

Faster way to start investing with outside capital

Way to build a track record (with outside capital)

Gain experience w/LPs & learn to operate (in some ways) similar to a traditional fund

Start building relationships with potential fund LP’s, VCs & founders.

Better pricing & flexibility of an SPV versus a traditional Venture Fund.

You can read our full post on this here titled “Leveraging SPVs to get to Fund 1” for this topic.

In summary, those who leave the syndicate ecosystem to raise a venture fund have in some regard graduated from the syndicate ecosystem (i.e the minor leagues) into the big leagues. So, while they may be gone (or less active) in syndicating deals, they have made it to the destination they were looking to achieve.

Congrats to the many people deploying capital out of their venture fund that started with SPV’s!

In SPVs, Only The Strong Syndicate Leads Survive

Given the drop off or the “graduation” to traditional venture funds, this leaves me to believe that the majority of the syndicate leads who are still remaining (from pre-2022) are indeed some of the top syndicate leads as it relates to consistency of bringing quality deals to the table and providing a positive LP experience. While there’s much more to it (i.e. IRR, MOIC, DPI etc.), in this shorter timeframe, I do think it’s a testament to those syndicate leads who have remained constant through the rapid market changes and shifts.

A lot of people say the best (or most followed) newsletters, podcasts, and social media influencers are those who simply remain consistent without giving up. I think part of this is true for syndicate leads as well. It’s a lot of work, it’s an absolute grind trying to make each deal happen, and working with a high volume of LPs with varying personalities/thoughts all make it a very hard job. Therefore, the syndicate leads who remain consistent over the years must be doing something right to survive and continue to put the work in to syndicate deals and successfully have LPs commit the amount necessary to invest in startups.

In many ways, this is similar to venture funds who go on to raise fund 2, 3, 4, 5 & beyond. Of course performance will vary, but if you get to fund 5, you are likely doing something right to have LPs enthusiastic to commit to fund after fund, after fund. In syndicates, the timelines are shrunk because there is no multi-year fund cycle, therefore syndicates will fall off quicker.

If you are not going gray after a few years of SPVs, you probably aren’t syndicating enough deals, just kidding…keep going :)

If you enjoyed this article, feel free to view our other referenced articles:

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!