- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- 💡5 VC Syndicate Learnings After Closing 500 SPVs

💡5 VC Syndicate Learnings After Closing 500 SPVs

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

July 10, 2024

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

Fill out our unique form to get to the top of the line here.

Deal Sheet = Access the Best (weekly) SPV Investment Opportunities @ Discounted Carry

This past Monday, we sent out Deal Sheet Issue #22, which included 4 new deals. Co-investors in Issue #22 included Nvidia, ICONIQ Capital, Lux Capital, Addition, DST Global, Ulu Ventures, Morgan Stanley, The Venture Collective, and many more!

To get access to these deals at 10% carry you can sign up for Deal Sheet here or book a call to learn more!

5 VC Syndicate Learnings After Closing 500 SPVs

We just closed and wired our 500th SPV at Calm Ventures; this is likely more than any solo GP entity globally (albeit we get a lot of help from external partners, VCs, etc.). Here are 5 key learnings from our experience over the last five years of putting SPVs together.

1. In SPVs, GPs are not Fund Managers

GPs running SPVs in VC are not fund managers. While we’re curating opportunities, syndicate leads do NOT control flow of capital; that is completely controlled by the SPV LPs, who can selectively choose which opportunities to participate in and which not to.

This has never been more clear in a down market (2023-2024) in which there’s a ton of demand still for “hot” opportunities such as OpenAI, Anthropic, etc. but relatively minimal interest in a large number of strong Seed to Series A opportunities, which in some cases, we feel as a cohort may outperform. Unfortunately in the SPV model, while we can do our best to outline why we believe these less buzzy opportunities are more interesting, SPV GPs don’t control funds. LPs are really their own fund managers.

This has been a wakeup call to me and a large number of SPV GPs; the number one reason I would slow down SPVs and move to a fund model is because of my increasing desire for full discretion over investment decisions, which are more aligned for outcome. Perhaps, LPs believe Syndicate GPs have that as we do bring deals of our choosing to market but this is not always the case. There is a sea of deals that we syndicated and canceled or didn’t bring to market altogether because of their lack of marketability (e.g. lack of tier 1 co-investor, traction, etc.) that most of our LPs require. And vice versa - there are GPs that may bring deals to market mainly because of their marketability.

It should also be a wakeup call for LPs in SPVs - you need a portfolio strategy to optimize your success, as LPs are their own fund manager. If you’re investing in early stage venture capital, I refer you to our prior article on LP strategy here.

This last point is self-serving but candid - learn, decide and optimize a portfolio and capital allocation strategy and use Deal Sheet to execute on your given venture strategy as Deal Sheet is meant to curate many of the most interesting startup opportunities and all of them have reduced carry attached to them, which you will likely be extremely thankful for on your winners.

2. The GP Carry Economics are Really Superior

On the plus side, the carry economics are arguably far superior for Syndicate GPs than the carry economics for fund GPs.

We previously put out an article discussing the economics of venture, and the reality is that while venture can be the best performing major asset class the returns are skewed to the top funds with the average fund barely returning 1x capital back. There is no major asset class that has dispersion of returns quite as high as venture capital.

This underscores the benefits for Syndicate GPs. For one, it means the time to actually receive carry income can be extremely quickly. Despite starting Calm Ventures in 2020, we had one nice exit in 2021 (~10x outcome in 12 months). While the returns from that investment were only ~10% of the capital deployed to that point, we still received carry (over a half million dollars). In a traditional fund if you returned only ~10% of capital back, you would not be seeing a dollar in carry from that sale.

To further underscore the GP benefit, as mentioned, around half of funds return <1x DPI. Meaning half of GPs aren’t seeing a dollar in carry from their funds. You can have a <1x fund in SPVs and still receive an enormous amount of carry distributions.

To take the extreme case, let’s say we invest $1M each into 100 investments via SPVs over the course of 3 years - so $100M invested total. 99 of those investments go to zero and one 100x’s or returns $100M. While LPs in aggregate didn’t make any money (we received $100M in distributions and invested $100M), the GP actually makes almost $20M dollars (20% carry x $99M in returns on the single performing investment).

It’s worth pointing out that while the carry economics are superior, the fee economics are substantially worse for Syndicate GPs, who often aren’t drawing any consistent income or salary.

3. This Ecosystem is Highly Cyclical

We deployed 3x the capital in 2021 than we did in 2023. That wasn't because we were doing any less deals or got smaller (in fact we got a lot bigger from # of LPs, brand, etc.), but it was because LP capital dried up. Most of the LP capital is retail related in SPVs, so when retail is generally doing well, as they were in ZIRP 2021 and the IPO market was completely open, there was a lot of VC interest from retail. In 2023, after multiple rate hikes, and a relative downturn in savings/macro, retail was less interested in taking a risk on approach.

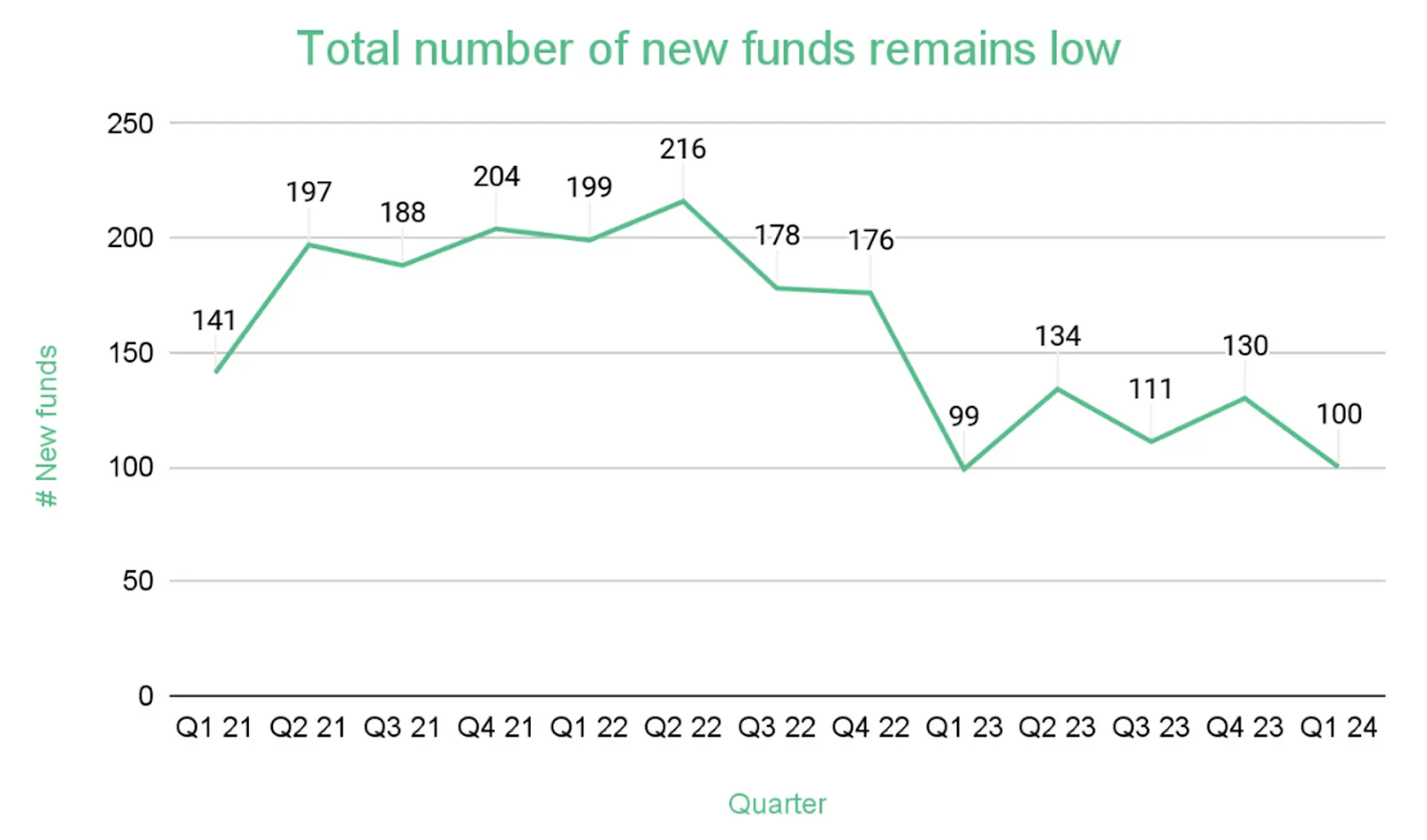

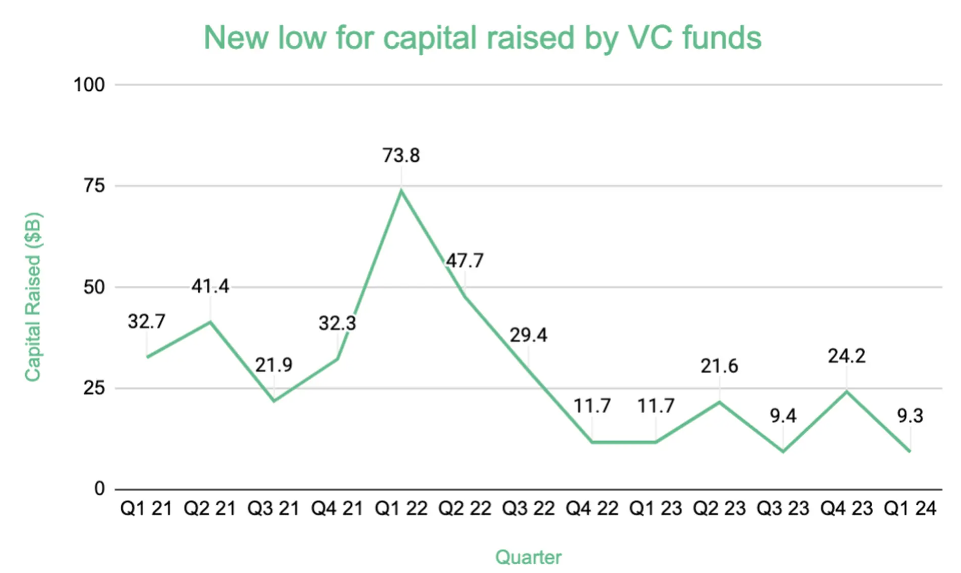

This isn’t completely unique to SPVs and is more broadly a venture problem. According to Juniper data, new fund creations continue to dwindle. This is likely worse than it seems as the industry is also going through consolidation with the mega funds taking up an increasingly large amount of the capital raised.

But I’d argue the impact hits harder in the SPV world. If you raised a venture fund in 2021/2022, you theoretically could meet the market where it's at, and deploy over an elongated period (3-4 year deployment period) and still have funds to take you through the venture downturn over the last few years.

As an SPV, once the market halts, the impact is felt more or less immediately; you have no fund capital or reserves to deploy and your business is entirely put into a standstill. This is a large reason why many of the venture managers who raised funds in 2021/2022 are still around and deploying, while the vast majority of SPV GPs I know have either halted running SPVs entirely or scaled their SPVs back 90%+. It is extreme.

What makes this more unfortunate is that 2023 will most likely be a better vintage for VC than in 2021 when multiples were at extreme froth. But due to structural dynamics with most Syndicate GPs running SPVs, this is a difficult problem to solve.

4. There are A Lot of Hacks to Scale SPVs Quickly

We previously put out a deeper dive on this topic in 2023 on how we scaled to 6,000+ LPs. You can read that here for a deeper dive. Now at >7,000 LPs in our syndicate, there are a ton of hacks to scale your SPV quickly including co-syndications, leveraging other Syndicate GPs distribution, generally doing high quality deals to get high word of mouth referral, building an active content/media brand, etc.

Despite having only a small handful of LPs when I first started doing SPVs, I understood (having been an LP in over a dozen SPVs) that there are hacks to scale the capital side, mainly the aforementioned ones. So if you have incredible deal flow, but no LPs, there are a large number of hacks to get started quickly.

With that said, having a lot of LPs doesn’t translate to high capital deployment in a down market. We also put out an article covering why the number of LPs is actually a vanity metric, so the better strategy may be to play the slow game and build meaningful close relationships, while simultaneously taking advantage of the growth hacks to scale your syndicate quickly.

5. SPVs are a Way to Move Fast, But Not a Way to Scale

I genuinely believe SPVs are the way to move extremely quickly, but difficult to scale beyond a certain point. There’s a reason why the largest venture capital managers have well over $40B in AUM and the largest VC syndicates globally likely are <$5B AUM. Most of the full time VC syndicate GPs I know have well under $50M AUM.

Why they’re great to move fast: I started in the syndicate ecosystem as a GP in 2020. At the time I had just finished a stint working for three years at an investment bank in San Francisco and was starting an MBA. I was five years out of undergrad at the time with no VC experience.

I dropped out of my MBA program fairly quickly (3 months in) and took a job at an awesome VC syndicate in LA (still to this day, I believe they are the #1 syndicate). After this internship, I went on to join a growth fund in LA in 2019, and then ended up leaving in 2020 to start Calm Ventures.

Despite having <1 year of paid VC experience when I started Calm (and I didn’t have the rockstar operating background), I still managed to start my own VC firm within 1 month of trying - in our first year we deployed $12M; in our second year, over $80M. If I were to have tried to raise a fund, it’s very likely at the time it would have been a 12-24 month process and I may not have gotten anywhere.

To summarize, syndicates are genuinely a great way to get started as they break down all the barriers of starting a VC firm. Unfortunately - they are not a way to scale for many reasons. Outside of AUM getting difficult to scale beyond a certain point and your investments highly dependent on the state of the market, I genuinely believe it is extremely hard to build a world class firm when the GP doesn’t own capital deployment. As mentioned, the LPs control capital, not the GPs, making it, in my opinion, extremely difficult to deliver outsized returns - from my experience LPs tend to invest heavily into hot deals and not extremely high risk pre-seed deals or lesser known companies where there “may” be more alpha. So over the long-run, I candidly think the main way to go world class is to start a fund.

If you enjoyed this article, feel free to view our other referenced articles:

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!