- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- xAI Didn't Prove the Model. It Broke It.

xAI Didn't Prove the Model. It Broke It.

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

April 11, 2026

In 2024, Elon Musk raised $6 billion for xAI at a ~$24 billion valuation. The company was barely a year old, had no meaningful revenue, and its primary asset was its founder's name. Two years later, SpaceX acquired xAI at a $250 billion valuation. On paper, it looked like a home run. In reality, it was a highly specific outcome produced by a largely unrepeatable set of circumstances. The consequence is the moment we're now living through: a flood of nine- and ten-figure seed rounds for AI companies that have, collectively, yet to prove a single one of them was worth it.

What actually made xAI work

Musk operates in a category of one.

He has a track record of many audacious bets that paid off — Tesla, SpaceX, and now xAI — giving him unlimited access to private capital at terms no other founder could extract and best in class labor. With a personal net worth well north of $100 billion, he also represents a form of perceived collateral almost no other founder can offer.

But even that wasn't quite enough. Strip out X's advertising and subscription revenue, and xAI was running at roughly $500 million in annualized standalone revenue against a reported cash burn of around $1 billion a month — with a portion of that $500 million in revenue reportedly coming from Musk's other businesses who were customers of xAI.

But the reality was the exit to SpaceX was a necessary strategic move and a balance sheet rescue at once.

Combining xAI's models with SpaceX's cash generation crucially solved the capital access problem that no further venture round could permanently fix and gave Elon investors another successful outcome. The deal was only possible because the same person controlled both sides of the table. The template is not really replicable.

For investors who got in at the $24 billion valuation, a $250 billion exit is roughly around 6x after dilution and more likely around 4-5x after fees and carry if you invested through a venture firm or SPV. That is a good outcome. It is not a generational one. It is not a fund returner. And it required everything to break perfectly for investors.

What the market heard instead

What Silicon Valley took from xAI feels worrying: that pre-product AI companies with star-pedigree founders deserve billion-dollar checks. The copycat class followed quickly — Thinking Machines Lab ($2B seed), Safe Superintelligence ($1B), World Labs ($1B), AMI Labs ($1B), humans& ($480M), Unconventional AI ($475M), and many others.

While early, none of these companies have generated meaningful reported revenue. Several have yet to ship a product. They are bets on founders — full stop. And while founder pedigree matters, it has never in the history of venture capital been a sufficient substitute for a business.

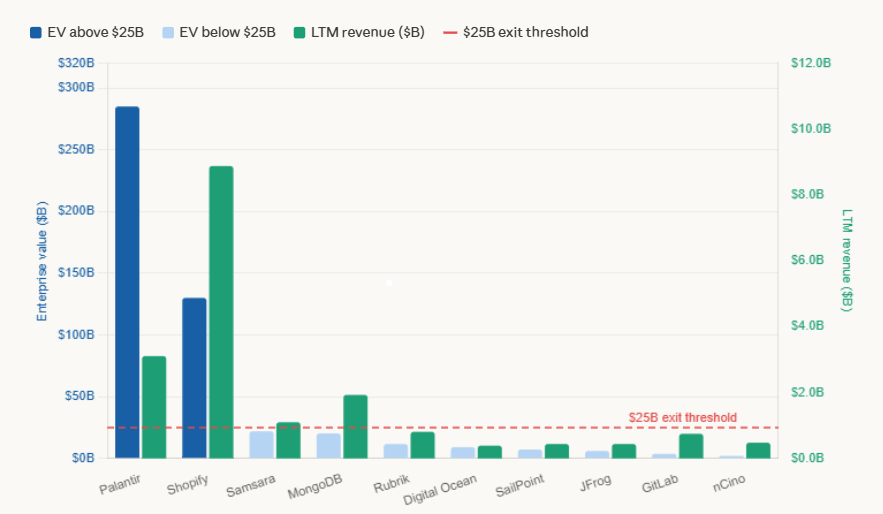

Here's the problem LPs aren't saying: at these entry valuations, the exit math becomes almost impossibly demanding. A $1 billion seed investment into a company valued at $5 billion needs a $25 billion exit just to return 5x gross — and that's before dilution, fees and carry.

The number of AI companies that will actually reach $25 billion in genuine enterprise value, through revenue and profitability rather than the next funding round, is much smaller than the number currently being funded at that premise. In public markets today, you need billions in revenue and roughly a billion in earnings to justify a $25 billion valuation as a software company. None of these businesses are close.

The median SaaS company today trades at roughly 3x ARR. Even the top five by ARR multiple — exceptional businesses — trade at around 16x. That means a company would need more than $1.5 billion in ARR just to reach a $25 billion enterprise value at a best-in-class multiple.

Companies like Samsara, Veeva, Zoom, and HubSpot can't clear that valuation bar — and these are among the best of breed publicly traded software businesses.

xAI's outcome success required a very specific buyer, with a very specific motive, controlled by the same person who founded the company and in a unique macro environment. That is not a comparable transaction. It is barely a market transaction at all. Using it as the benchmark for what a billion-dollar AI seed round can return is using a one-of-one outlier to justify an investment thesis.

How this probably ends

A small number of the current mega-seed class — perhaps two or three — will find genuine product-market fit, build durable revenue, and return some small multiple of capital.

The rest will likely return <1x. That outcome, while painful for individual LPs, is at least a known risk of the asset class. What's different this time is the entry price. When funds are paying $5 to $12 billion at inception for companies with no product and no revenue, the math requires outcomes that the entire history of the software industry suggests are rare to the point of being theoretical.

The reckoning will likely come one of three ways. Public outcomes fail to match private markups — as we saw play out brutally across SaaS in the last cycle. Macro turns and capital markets go risk-off — as happened in 2022-23, when growth-at-any-price became a liability overnight. Or the capital markets for these businesses simply dry up, forcing the question of whether any of them can stand on their own.

Which brings us to the bigger question: why does this keep happening?

The answer is largely that the people underwriting the risk and the people bearing it are not the same people.

In the SPV and co-investment ecosystem especially, LPs are often calling their GPs asking to get into these deals. And under normal circumstances, that instinct makes sense. SPVs work when upside is asymmetric — when a single winner can return 10x, 50x, or 200x on invested capital, the structure justifies the concentration.

The problem is that these deals have already compressed that asymmetry at entry. When you're investing into a $5 to $12 billion valuation with no product and no revenue, the realistic ceiling on a great outcome is 5x — and that's before fees, carry, and dilution. That's not an SPV return profile. That's a late-stage growth equity return profile, without the downside protection that typically comes underwriting a mature business.

So what are we doing?

We'll keep offering these deals. LP demand is real, the pipeline exists, and the honest truth is that one or two of these deals will likely find genuine product-market fit and return 5x or better. And as a Syndicate GP, that model works for us.

But if I were sitting on the LP side of the table, unless the founder is a category-of-one operator (e.g. Musk), I’d be passing on anything where the first institutional check into the business is already in the billions. The entry price has already done most of the damage and the asymmetry that makes venture work is likely already gone. Follow the Last Money In authors on LinkedIn