- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- Why Startups Are Shutting Down in Droves

Why Startups Are Shutting Down in Droves

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

October 30, 2024

🚀 Unlock Elite Startup Deals without an upfront commitment! 🚀

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

Fill out our unique form to get to the top of the line here.

Deal Sheet Free Trial. Start your 7 day trial here!

Deal Sheet provides accredited investors:

Access to some of the best startup opportunities across the VC syndicate ecosystem (est. 150-200 deals on Deal Sheet per year) and

All Deal Sheet deals come at discounted carry – all opportunities on Deal Sheet are listed at 10% carry (versus 20% standard) with select opportunities (at our discretion) at 0% carry.

Try the free trial today here!

Why Startups Are Shutting Down (Right Now) in Droves

The startup landscape is experiencing a seismic shift. In Q1 2024 alone, 254 venture-backed companies went out of business, many of which have previously achieved nine figure valuations. Just last week brought a sobering cascade of LinkedIn posts: founders of AI startups, direct-to-consumer brands, and fintech platforms all penning heartfelt goodbyes to their teams and customers. These weren't just failures—they were casualties of a fundamental market reset that's forcing us to reexamine how we build and value early-stage companies.

The reality is that the past couple of years have been a rollercoaster for the global economy and startups that raised venture capital. We've emerged from a bear market that saw significant downturns in public equities, cryptocurrencies, and other asset classes. This market downturn has had a ripple effect on the startup world, creating a challenging environment for startups to navigate and/or stay afloat.

In this post, we’ll cover the aftermath of the bear market we are seeing play out in real time. This aftermath has led to so many startups shutting down or being acquired for pennies on the dollar and we aim to explain a lot behind all of this and what it means for the startup ecosystem.

The VC Funding Crunch: A Drastic Shift in VC

The venture capital landscape has shifted dramatically since the start of 2022, leaving many startups that previously raised at sky-high valuations in a precarious position. This "funding crunch" is reshaping the startup ecosystem and forcing companies to adapt or face dire consequences. Those that have not or could not adapt are the ones we are seeing go out of business at a rapid pace presently.

Before we jump into why the funding crunch is taking place and what that means, it is important to realize the consequences of being overvalued in a previous round (and previous market). For the many companies that raised during this couple year period, it seemed great at the time, but the reality is that in this new market, the overvalued startup is now:

Having difficulty raising new funding

Experiencing pressure to meet unrealistic expectations

Limited or minimal upside for potential investors and founders

Increased risk of down round (bad signal & dilutive)

Challenges in attracting strategic acquirers

So what caused this funding crunch?

Market Reset: The tech valuation bubble has burst, with SaaS multiples dropping from 25x-50x+ to 5-10x ARR. Public comparables have forced private markets to drastically adjust expectations, particularly impacting growth-stage valuations and late-stage fundraising.

Macro Headwinds: Aggressive Fed tightening and persistent inflation have ended the zero-interest-rate era, fundamentally shifting investor risk appetite. The flight to quality and safety has disproportionately impacted venture-backed startups reliant on cheap capital.

Profitability Premium: The "growth at all costs" era is dead. Investors now demand clear paths to profitability, sustainable unit economics, and efficient capital deployment. Companies with strong gross margins and capital-efficient models command significant valuation premiums.

AI's Creative Destruction: The emergence of foundational AI models is obsoleting traditional SaaS plays. VCs are rapidly repositioning portfolios toward AI-native companies, leaving legacy software businesses struggling to remain relevant and attract capital.

Public Market Outperformance Challenging Private Value Proposition: The traditional illiquidity premium in private markets has been significantly challenged as public markets, particularly in tech, have delivered strong returns with immediate liquidity. Companies like Nvidia, Meta, and Microsoft have generated venture-like returns (100%+ in 2023) while offering daily liquidity, making it harder for VCs to justify the 7-10 year lock-up periods typically required for private investments.

Lack of Distributions Straining LP Confidence: Limited Partners (LPs) have experienced a severe slowdown in distributions from their VC portfolios due to the challenging IPO and M&A markets. With IPOs at historic lows and holding periods extending beyond traditional timeframes, LPs are facing a "denominator effect" where their private market allocations are overweight due to both reduced public market valuations and lack of realizations. This has forced many LPs to slow or pause new commitments to maintain portfolio balance.

💵 Last Money In Deals: We have made over 800 startup investments. Accredited investors & qualified purchasers within the LMI community can now gain access to our alternative investments such as venture, late-stage growth, and private equity through our deal flow sheet. Interested (it's completely free)? Fill out this form.

💰Reader Survey: As part of our valued readership, we’d love to get to know you more. Help us understand our fast-growing audience of 50,000+ by completing this quick survey. To show our thanks, two participants will receive a $100 gift card." 1 minute survey here.

👜Try Deal Sheet for Free: Want to join hundreds of subscribers in trying Deal Sheet, our premium newsletter that provides you access to the top venture deals with discounted carry. Try Deal Sheet for free for 7 days here.

🐦 Follow Us: Visit Alex’s Linkedin and Zach’s X account for constant updates on all things venture capital, SPVs and more!

The Valuation Dilemma: Raised at a high valuation, so now what?

There were so many SaaS, ecomm, fintech and other startups that were able to raise capital quickly, and at high valuations (2x, 5x, 10x, 50x of what they’d be valued in today's market). I’m not going to pretend our syndicate did not participate in many of these rounds and companies… we did. We invested alongside all the tier 1 VC’s (and backed great founders) out there during this time while the capital was flowing and we did not see a sharp turn right around the corner.

But now those same companies find themselves in extremely difficult funding environments and situations. These startups that raised at exceptionally high valuations during the bull market are facing many unique challenges today including:

Valuation Mismatch → Current market conditions often don't support previous valuations, leading to potential down rounds or in many situations small internal rounds or no rounds because founders and existing/new investors cannot agree on terms. To take an example - Peloton at one point was valued at around 23x sales; today it's achieving a 0.85x sales multiple or almost 97% multiple compression.

Higher Bars for Growth → To justify their valuations, these companies need to demonstrate exceptional growth and progress. Most of these companies are trying to figure out how they can get back to their recent valuation in 1-3-5+ years with limited capital needs i.e. do it without heavy dilution. This is incredibly hard mentally but also to grow at a similar pace but with way less resources after likely cutting burn significantly.

Burn Rate Pressure → High valuations often came with high burn rates, which are now unsustainable in the current climate. Most companies flipped the switch and performed massive budget cuts and got rid of many employees, to as quickly as possible, figure out how to get to profitability or extend their runway many years down the road. Those that could not do this either massively diluted themselves or went out of business.

Investor Expectations → Previous investors may be resistant to lower valuations, complicating new funding rounds. I’ve seen a lot of friction between founders and VCs now. Many founders are now upset that they sit in cap table purgatory even when the VC’s agreed to these terms previously. I’d also imagine (and have seen) a bunch of VCs stepping up to lead internal bridge rounds to help extend runway to get to the next milestone, next funding, or profitability. With this rapid shift in the economy and venture landscape, a lot of decision making relies on the founders and VCs agreeing on the path forward. This is a very hard task. While this has likely led to many negative relationships between founders and VC’s, I think there are also a ton of VCs who have truly been helpful to navigate this time with portfolio founders or help find a soft landing for the business.

See below for a few examples of some of the once high-flying companies that were able to secure a bunch of venture capital and likely growing rapidly that were unable to turn it around when the market changed up immediately on them.

Fast

Fast, a one-click checkout startup, raised $125 million in funding from investors like Stripe and Index Ventures. However, it shut down entirely in 2022, unable to sustain its high valuation and burn rate. Fast had aimed to transform online shopping but ultimately failed to gain enough traction to justify its lofty valuation.

Zume

Zume, a robotic pizza delivery startup, raised nearly $500 million at a valuation of over $1 billion. The company shut down in 2022 after pivoting multiple times, struggling with technological difficulties, and failing to achieve profitability. Despite its massive funding, Zume was unable to create a sustainable business model.

ScaleFactor

Accounting software startup ScaleFactor raised $104 million from prominent investors like Bessemer Venture Partners and Coatue Management. The company shut down in 2020, just months after raising a large round. ScaleFactor reportedly used aggressive sales tactics and prioritized fundraising over product development, leading to customer dissatisfaction and eventual failure.

Olive AI

Healthcare AI startup Olive raised funding at a $4 billion valuation in 2021. However, the company struggled to live up to its lofty valuation and shut down in 2023. Olive's technology reportedly fell short of expectations, and the company burned through cash trying to achieve unrealistic growth targets.

Convoy

Digital freight startup Convoy raised funding at a $3.8 billion valuation in 2022. Despite the high valuation, the company shut down in late 2023, unable to secure additional funding or achieve profitability in the competitive logistics market.

These examples highlight how overvaluation during the 2019-2021 funding boom led many startups to take on unsustainable burn rates and growth expectations. When market conditions changed and funding became scarce, the fundamental flaws in these businesses were exposed, and they were no longer able to justify their high valuations or raise additional capital at terms that made sense for everyone, ultimately leading to their shut down.

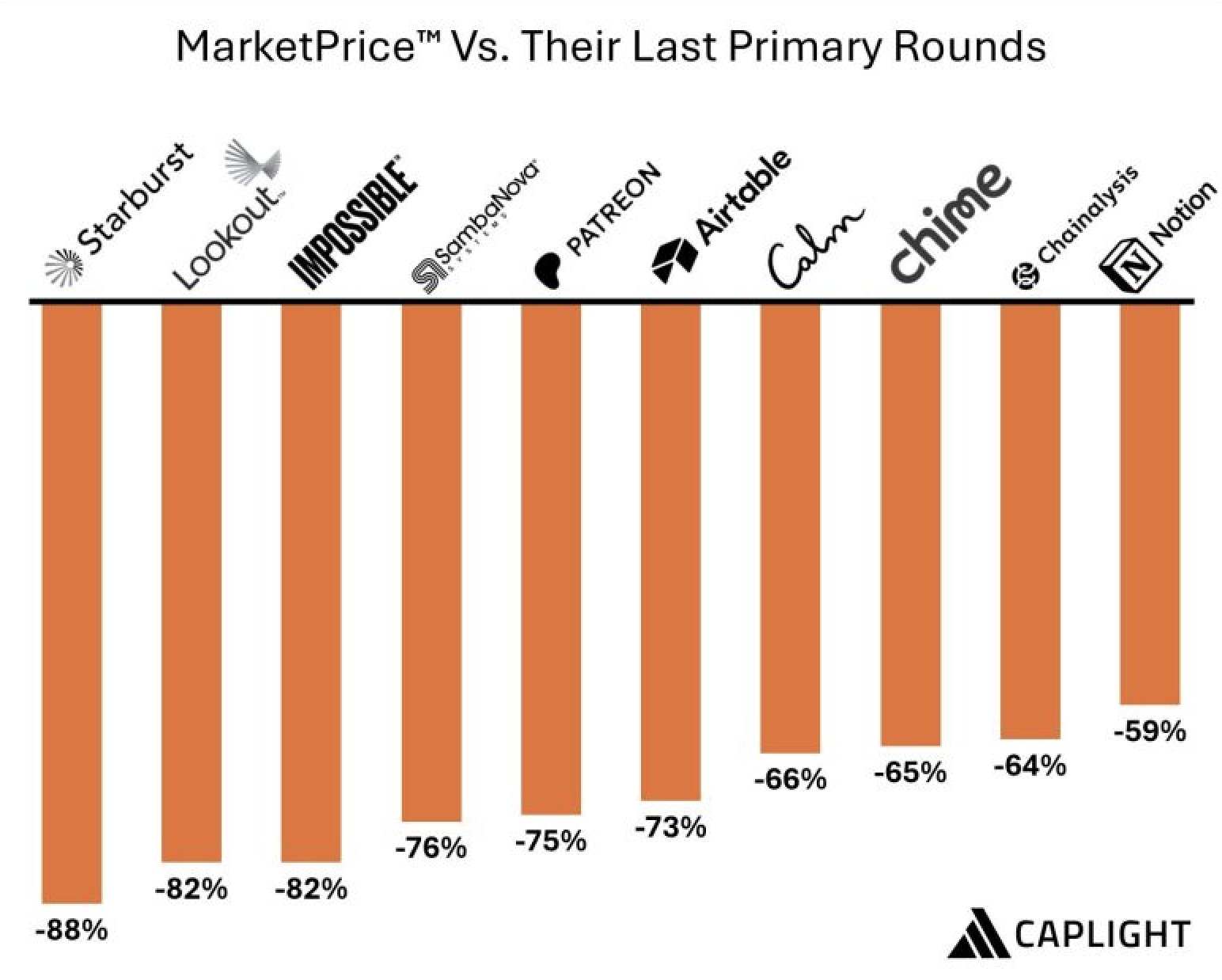

Zombiecorns: A Tale of Forgotten Unicorns

I saw a funny new term called “zombiecorns” (shown above) by our friends at Caplight recently. While these companies have not gone out of business (and we have no reason to believe they will), a few may be in a cap table purgatory position in that they can’t justify last round’s pricing and have raised too much capital relative to their true valuation, making fundraising prospects tricky. It’s still TBD on where these companies land but they likely suffer to some capacity from the same previous market shift that many of the companies that went out of business did.

Many of these companies are actively trading on the secondary market at discounts between 59% to 88%, a massive discount from their peak.

My Founder Sympathy

Some of this is just simply bad market timing for founders. I’d bet some of these folks would be crushing it if they had simply started their company 2-3 years later and raised normal amounts of capital and fair valuations.

Put yourself in the founder's shoes for a minute. What are you supposed to do if it’s going to take 5+ years to raise another round back at par with the round you raised 2 years ago? That’s incredibly tough mentally to reset expectations and spend more than 3 (or more) years just getting back to the valuation you were at.

Whether it’s the mental challenge or the tightened budgets companies have now, many will not be able to achieve this while keeping their employees motivated and part of the team. Oh right… as founders it's not just about you staying motivated to “get back” to where you were. You need to convince everyone in the company to stay motivated on the mission even after many of their colleagues may have recently been let go.

This is a huge uphill battle.

Founders realize they may never be able to raise an up round again. Many of them have a bad taste and are probably trying to figure out how to get to profitability and never have to raise from a VC or outside investors again. There is not a simple answer here on what you can do and how you can keep your team motivated and investors excited about their potential return.

Conclusion

The 2024 funding reset isn't just another dip in the venture cycle—it's a fundamental restructuring of how startups are built and valued, at least for all companies outside of AI, which are still receiving very frothy multiples. This correction, while brutal in its swiftness, is forcing a return to first principles: sustainable unit economics, disciplined growth, and genuine product-market fit. For every founder currently navigating these turbulent waters, the message is clear: the era of growth at all costs has ended, replaced by an environment where capital efficiency and strategic resilience matter.

If you enjoyed reading this article, feel free to view our prior articles on deal structures and terms:

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!