- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- VC Uncapped Rounds - Invest or Avoid Completely?

VC Uncapped Rounds - Invest or Avoid Completely?

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

April 03, 2024

Last Money in is Powered by Sydecar

Sydecar is a frictionless deal execution platform for emerging venture investors. We make it easy for anyone to launch SPVs and funds in minutes, with automated banking, compliance, contracts, tax, and reporting so that customers can focus on making deals and building relationships.

Deal Sheet = The.Best(& investable).Deals.Period.

Curated & Discounted SPVs directly to your inbox

Deal Sheet is a paid weekly newsletter that delivers the best startup investment opportunities weekly. These deals are being syndicated by 20+ of the best and most active syndicate leads we’ve worked with. All Deal Sheet deals include discounted carry (10% carry versus standard 20%).

In March, 17 deals were shared via Deal Sheet. On Monday we shared five new opportunities for paid subscribers, including:

Deal #1 → Series A (led by a Peter Thiel fund) members-only concierge + charge card for high net worth spenders

Deal #2 → Union Square Ventures backed electricity provider

Deal #3 → Current YC (W24) batch company building a platform that helps asset managers modernize fundraising via AI-powered automations

Deal #4 → Fast-growing AI pilot defense technology company

Deal #5 → Leading Andreessen Horowitz backed digital banking platform

***If you are interested in becoming a Deal Sheet subscriber, but want to chat further, email us here directly ***

VC Uncapped Rounds - Invest or Avoid Completely?

An uncapped financing round, usually in the form of a Convertible Note (short term debt that converts into equity at a future date) or a SAFE (simple agreement for future equity), is a type of convertible security that is commonly used by startups to raise financing from venture capitalists or other investors.

An uncapped note or SAFE typically has the following key features:

Convertible: It is a form of debt (Note) or contingent equity (SAFE) that can be converted into equity (shares) in the company at a future priced round of financing (e.g. Series A preferred equity round) or liquidity event (e.g. acquisition or IPO).

Uncapped: There is no predetermined valuation cap on the conversion price. This means that when the Note or SAFE converts into shares, the investor's stake will be determined based on the valuation of the priced round, without any maximum valuation limit.

Discount: Often, but not always, uncapped notes or SAFEs include a discount rate (e.g., 10%, 20%, etc.), which gives the investor a discounted conversion price compared to the new investors in the priced round. If the next round takes place at a $100M valuation and your uncapped structure comes with a 10% discount, you should theoretically be converting at a $90M valuation.

The uncapped structure is in contrast to priced preferred equity financing, which have a specific valuation and price per share attached to it, meaning in “priced” rounds investors know the price per share and valuation (or implied valuation) that they are acquiring shares at. In an uncapped round, VCs are investing without this price certainty.

Generally, VCs prefer not to invest in uncapped rounds when investing in startups. In fact, many will never invest in an uncapped round. The main reasons are lack of valuation limit / lack of price certainty and the perception of not being rewarded properly for the risk the VC is taking on in this structure. In an uncapped round, there is no predetermined valuation cap on the conversion price when the investment converts to equity, meaning that if the startup raises a subsequent priced round at an exorbitantly high valuation, the VC will have converted at a price far higher than they expected to. Additionally, an uncapped round today could make future priced rounds more challenging by creating misaligned incentives among investors with different entry valuations.

Uncapped Notes or SAFEs are fairly uncommon, but I have put together SPVs for a few.

From my experience, uncapped structures are typically done by startups that have 1) enormous leverage in negotiation as they don’t need additional financing or have large excess demand and thus can dictate more difficult terms for VCs or 2) are an insider led bridge round to help their portfolio company make more progress and overall be in a better position to raise a larger priced round (e.g. Series A, B, etc. typically). In the 2) example, the VCs leading the uncapped round usually have already acquired a meaningful ownership stake, and in these situations would prefer to help the company be in the best possible position when raising its large next priced financing.

Brought to you by Hiive

*Investing in private securities involves a high level of risk.

Whether you’re a fund manager or solo investor, Hiive gives you access to some of the most exciting private companies in AI and Web3, including the likes of Anthropic, Rubrik, SpaceX, Kraken, and Groq. Better yet, you get troves of historical pricing data based on real user activity across hundreds of the top unicorns for free.

Create an account today and learn why thousands of the top investors trade on Hiive.

So in what circumstances would I “consider” investing in an uncapped financing?

Large Existing Stake: If I already have a significant equity stake from prior priced rounds, I may consider an uncapped Note/SAFE as a smaller bridge investment to extend their runway and help put the portfolio company in the best position to raise its next priced financing.

Access to a Top 1% Startup: In cases where a startup is doing exceedingly well (top ~1% startup) and my only way to get access to the opportunity and build a relationship with the company is through an uncapped round, I may take that opportunity to get exposure even without formal valuation certainty. Of note, in these investments, I would likely require 1) a discount to the next round (10-35%) and/or 2) some certainty that the next financing would happen within the next 12 months (the sooner the better).

Large Discount with Huge Assurances of Near-Term Financing: While uncapped is not ideal, a large discount offers a built in markup, which can be lucrative especially if there is a near term financing. For example, if a company gets valued at $100 million but a VC invested in an uncapped SAFE with a 20% discount just a few months earlier, the investor's markup is already 1.25x in months just due to that discounted entry price compared to the priced round. Not bad…

It’s worth pointing out that I’m making these statements as an Syndicate GP, not a fund GP.

The reality is the syndicate structure is more flexible - we do not have ownership requirements, or fixed amounts of capital. We theoretically have infinite capital and can do as many deals as we raise for - we discussed this in detail in our article How We Invest in Over 100 Startups a Year as a Syndicate and Why Most Funds Can’t.

I think generally traditional funds are more wary of investing in uncapped structures, which was validated in my replies from the fund GPs (among other conversations) on the topic. For funds I “most often” see them participating in uncapped structures for existing portfolio companies that they’re looking to bridge for the next larger priced round.

In what scenarios would I rarely/never invest in an uncapped structure?

Basically every other round that didn’t meet the criteria above…but clear no’s include:

No Discount: There was only one startup that I ever invested in who raised at an uncapped structure with no discount, and candidly it left a horrible taste with me. The startup in this situation is basically asking the VC to take all of the risk without any of the near term upside as you're guaranteed no appreciation from this point until their next financing. An exception would be if the company was in the process of negotiating Term Sheets with price certainty on our end (e.g. about to close a preferred round).

Any Non-Top Business That Wasn’t an Existing Port-Co: I wouldn’t invest in an uncapped structure for a business that wasn’t a top quartile performing startup (generally).

Have any uncapped investments worked out for me so far?

We’ve done a few uncapped investments over 450+ SPVs and candidly most have worked out for us so far (but to underscore, we are passing on the vast majority of them). We invested in a Seed+ round that converted at a meaningful discount in a strong Series A. That Seed+ investment also allowed us to build a relationship with the company that enabled us to follow-on in the Series A round. We invested in an uncapped into a strong growth round; that company later got acquired for a nice premium to our conversion price. There are others.

We asked several GPs how they think about uncapped structures and in what situations they would invest in them. Here are their replies:

Zach Coelius, Coelius Capital - "The only way I have ever seen an uncapped investment make any sense is if it is a very large shareholder offering a small check to bridge to a large financing. Otherwise they are honestly one of the dumbest things in venture.”

Marshall Sandman, Animal Capital - “We would never invest in an uncapped note. I can’t think of an exception. I don’t understand why a sophisticated investor would ever accept it.”

Dan Engle, Santa Barbara Venture Partners - “We would never do an uncapped note. We passed on one last year that was a great fit in every way except that they wouldn't put a cap on the note. It's a deal breaker for us and for the VCs we know. But some angel investors seem to be willing to accept it. I can’t see why anyone would buy an illiquid private company stock (or most any investment) not knowing more or less what price they're paying for it.”

Aidan Gold, Hyperguap - “Uncapped SAFEs are terrible for investors as you don't know the price you're paying for a startup and the next investor who prices the round could be completely irrational and make the price very high. I usually avoid them, but we have done an uncapped SAFE since the prior round was extremely competitive and we were unable to get our full allocation in, and we thought the next round would be extremely competitive as well. We got a discount for investing early and wanted to guarantee we got in. The board didn't want to give a new price between financings, so they told the company to do uncapped and let the next round lead determine the price.”

Jeroen Bertrams, DVC - 1) What do you make of uncapped structures (e.g. uncapped notes, uncapped safes)? => “We tend to skip these rounds, with some exceptions.” 2) In what scenarios do you most often see uncapped structures? => “When companies are close to a new round, they do not want to send any valuation signals to VCs. In these cases, companies sometimes choose to offer uncapped rounds.” 3) In what situations would you invest in one (if any) and when would you avoid them? => :Only when we believe that the company will end up doing very well, and only in case there's a significant discount. Risk-reward balance should be reasonable” 4) Have any uncapped investments led to a very positive outcome for you? => “Tough to say; we only did a few and so far those companies are doing alright.”

Notably, VC lawyer Chris Harvey provided us evidence with a contrarian and more nuanced take on the matter.

“Everyone assumes a valuation cap is always more investor-friendly than an uncapped SAFE, but that's not true.

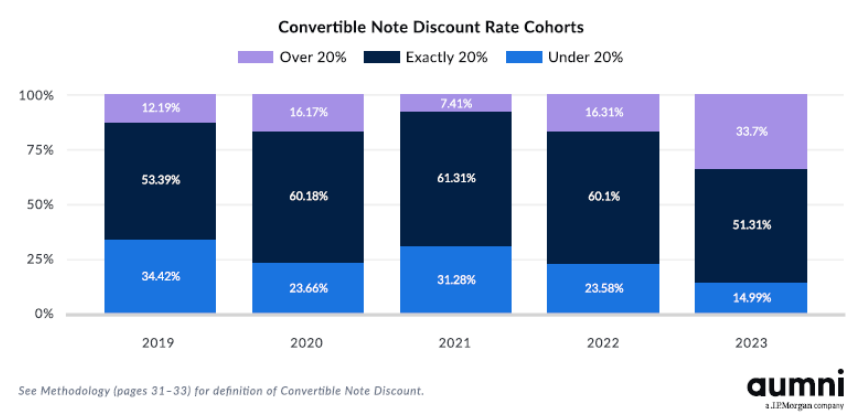

In 4Q 2023, Aumni reported that 30% of all bridge rounds were on caps lower than the pre-money valuation of the immediately preceding round. If you invested on a post-money Safe valuation cap of $10 million, and the next round's pre-money valuation is only $12 million, you would have been better off investing with an uncapped Safe at a discount of 20%+. That's because the break even point is:

$10 million / (1 - 0.20) = $12.5 million; Any pre-money valuation above that number, then the valuation cap should apply, but below that break even point, the discount should apply

When it makes sense to apply a discount over a valuation cap: Discounts Increasing (20%+): Discount rates are increasing - Aumni shows Discounts over 20% more than doubled from 16% in 2022 to 34% in 2023. 85% had a discount of 20% or more.”

To summarize:

Uncapped financing rounds do not have a predetermined valuation cap, meaning investors' stake will be determined based on the valuation of the next priced round, without any maximum limit.

Venture capitalists generally, but not always, avoid uncapped rounds due to the lack of valuation/price certainty, which could result in paying more than expected.

As a syndicate GP, I would “consider” an uncapped round under certain circumstances:

If I already own a meaningful equity stake and the uncapped round comes with a large discount that will put the company in a strong position for its next priced round.

If it's a top ~1% startup and the uncapped round is the only way to gain exposure.

If it's a high performing startup and there's a meaningful discount and assurance of a near-term (<12 months, ideally <3-6 months) priced financing with valuation certainty of that round.

Scenarios where I would rarely/never invest in an uncapped structure:

No discount is offered.

Any non-top performing company that’s also not a portfolio company

Traditional venture funds are generally much more wary of uncapped structures than syndicates (myself) by nature of their constraints and structure. The most common scenario I see a fund VC invest in an uncapped structure is to bridge an existing portfolio company to the next priced round, but many VC funds will never invest in an uncapped structure.

Contrary to the perception that uncapped structures are unfavorable, there is data that suggests this may not always be true. In 4Q 2023, Aumni reported that 30% of all bridge rounds were on caps lower than the pre-money valuation of the immediately preceding round. Meaning if you invested on a post-money Safe valuation cap of $10 million, and the next round's pre-money valuation is only $12 million, you would have been better off investing with an uncapped Safe at a discount of 20%+. We believe this suggests it is important to approach the topic with much more nuance then is typically done.

If you liked this article, feel free to view our past articles on VC structures.

Last Money In is Powered by Sydecar

Sydecar is a frictionless deal execution platform for emerging venture investors. We make it easy for anyone to launch SPVs and funds in minutes, with automated banking, compliance, contracts, tax, and reporting so that customers can focus on making deals and building relationships.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!

✍️ Written by Zachary and Alex