- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- Venture Math Is Breaking

Venture Math Is Breaking

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

March 14, 2026

Venture Math Is Breaking

If you've been in and around venture the last decade, venture math has gotten harder. Deals are harder to win. Prices are higher. Distributions take longer. Disruption is killing other startups faster. The venture market has fundamentally shifted as the asset class matures. Now we have the data. A benchmarks report from AngelList covering 1,000+ venture capital funds with performance data current as of January 2026 puts hard numbers behind what many of us have been feeling.

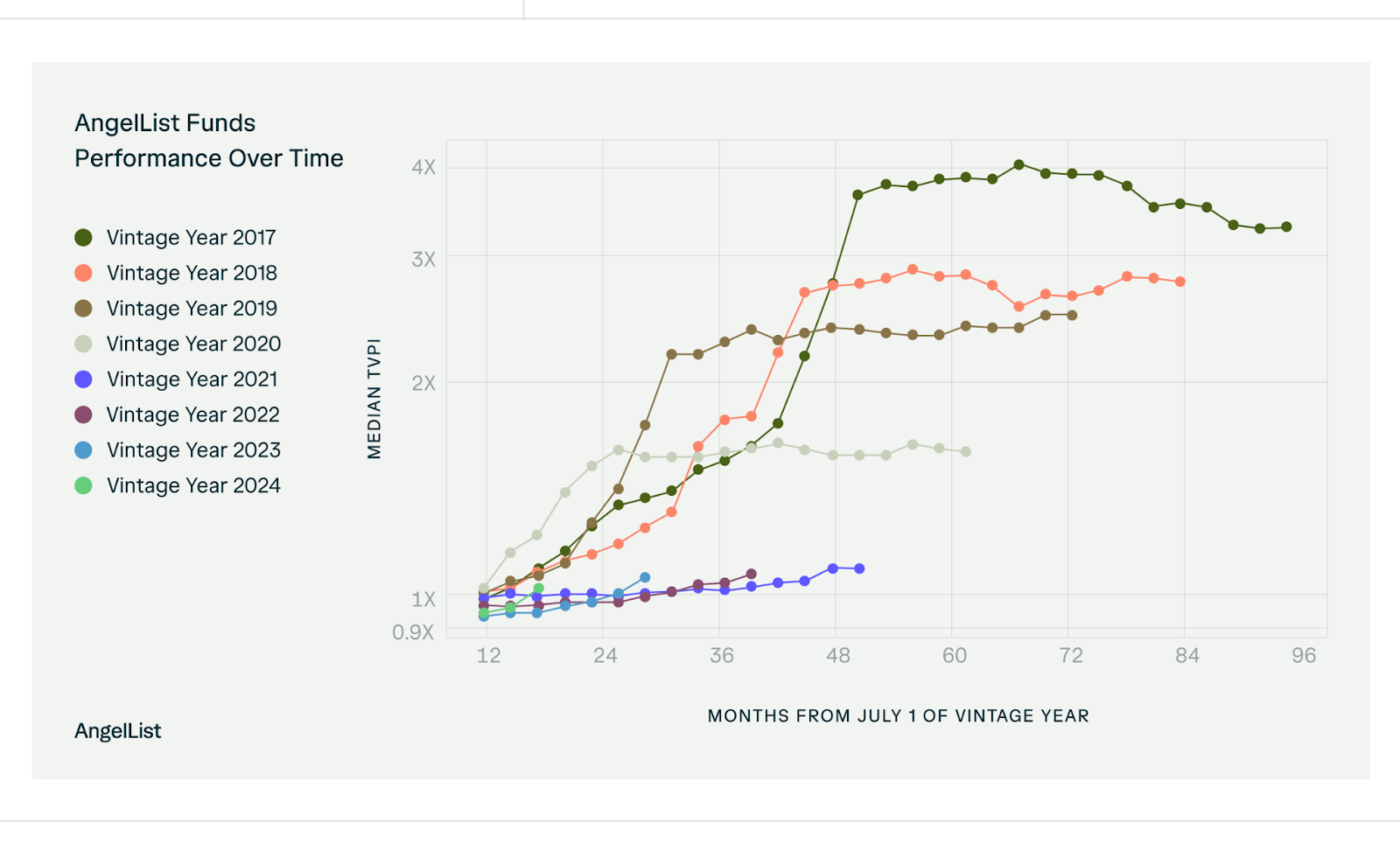

When you plot median TVPI over time for each vintage year since 2017, you'd expect each to follow its own trajectory — after all, each year's funds are investing in completely different companies. But that's not what happens.

Median TVPI over time by vintage year. The 2021-2023 vintages (bottom cluster) barely move off the 1.0x line.

The vintages from 2017-2020 show a similar pattern: a sharp spike in TVPI occurring at the same calendar time — late 2020 through early 2022 — then flatlines. The 2017 vintage jumped from ~1.75x to 2.74x. The 2019 vintage went from 1.27x to 2.18x. Same window. These markups weren't driven by individual fund strategy or stock-picking — they were driven by a market-wide repricing event fueled by zero interest rates and crossover capital flooding into venture. When the tide went out, everyone's portfolio froze.

Now look at the 2021-2023 lines. They barely move off 1.0x.

The 2021 vintage at 54 months sits at ~1.09x median TVPI.

The 2019 vintage at 42 months was at 2.37x.

The 2017 vintage at 54 months was at 3.66x.

The recent vintages aren't just underperforming in absolute terms — they're dramatically behind where prior vintages were at the exact same point in their lifecycle. And the gap keeps widening.

But here’s the catch and what makes the data even more interesting: a lot of those 2017-2020 TVPI numbers are probably heavily overstated.

Look at the chart again — the massive spikes for those vintages all happened during the same COVID-era window when valuations went haywire. Many of those markups were based on frothy late-2020 and 2021 financing rounds that priced companies at levels we now know weren't sustainable. If a seed-stage company raised a Series A at a $200M valuation in mid-2021, the fund marks that position up accordingly. But if that company hasn't raised since — and many haven't — it's still sitting on the books at that inflated mark.

The reality is that a huge number of these portfolio companies will never raise again at those prices. Some have done down rounds. Some are quietly dying. But until a new priced round forces a re-mark, the TVPI stays frozen at the peak.

So when you see a 2019-vintage fund showing 2.48x TVPI, ask yourself: how much of that is real, and how much is a stale mark from a round that priced in a completely different world? If you repriced those portfolios to today's market, the 2017-2020 vintages would likely look materially worse — which means the "good" vintages (2017-2020) and the "bad" vintages (2021-2023) may all be bad vintages.

The whole asset class may be sitting on more unrealized losses than anyone wants to admit. 2024 is starting to look a bit better than the 2017-2020 vintages at the same period, but candidly it is too early to say.

Too Much Capital, Not Enough Great Deals

The performance problem in my view is mostly structural.

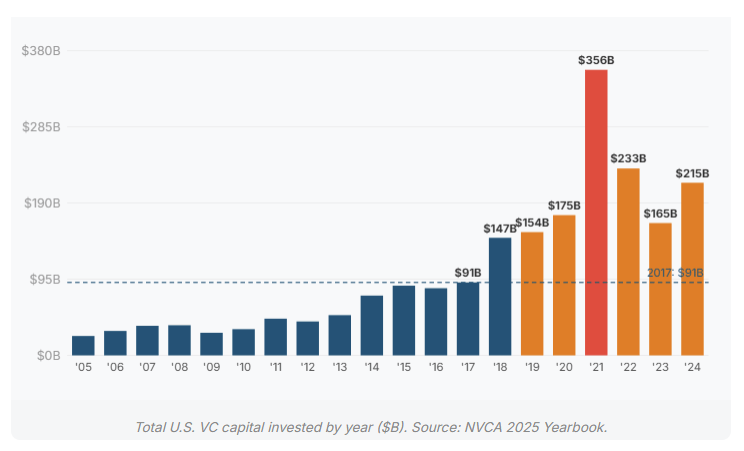

There's way too much capital chasing too few quality deals, and it's been driving entry prices up across the board and across rounds for years. Look at this chart. Total U.S. VC invested went from $91B in 2017 to $356B in 2021 — nearly a 4x increase in four years. Even after the correction, 2024 still saw $215B deployed. That's more than double what was invested annually just seven years ago and 9x what we say 20 years ago.

When dozens of funds compete for allocation in the same round, entry valuations get bid up. A company that would've raised at $10M post-money in 2018 can now command $25-30M for comparable traction. The math is unforgiving: pay 2.5x more on entry, you need 2.5x more exit value to generate the same return.

And here's where the squeeze really tightens — exits have dried up at the same time entry prices went up. The IPO window has been largely shut since late 2021 for venture-backed companies. M&A has been constrained by antitrust scrutiny and higher rates making leveraged buyouts more expensive. Companies that would have gone public 3-4 years ago are staying private indefinitely, doing down rounds, or limping along.

This is exactly what the DPI numbers reflect. When the pathway to exit is blocked, cash doesn't come back to LPs. And when cash doesn't come back, the whole flywheel slows: LPs who aren't getting distributions become reluctant to make new commitments. GPs who can't point to realized returns struggle to raise successor funds.

So When Does This Get Better?

Honestly? I'm not sure it ever does — at least not anytime soon.

We've seen this movie before in other asset classes. Hedge funds were printing money — then capital flooded in. By the mid-2010s, the average hedge fund wasn’t beating a basic index fund, and the industry went through years of painful consolidation.

Private equity followed a similar arc. Early LBO funds generated outsized returns buying companies cheaply with available leverage. Then every pension fund and endowment wanted PE exposure. Dry powder ballooned, purchase multiples climbed steadily, and median returns compressed. The top quartile still does well — but the asset class broadly got harder as it got bigger and more competitive.

Now it's venture capital's turn. And arguably crypto funds too, which saw the same cycle play out even faster — massive early returns attracting a flood of capital, compressing the opportunity for everyone who showed up after the first wave.

The pattern is always the same: an asset class generates outsized returns, capital rushes in, competition drives up prices, and the structural alpha that made the early vintages special gets arbitraged away. It doesn't mean nobody makes money — the best funds in every asset class still outperform. But the gap between median and top decile fund becomes the whole game, and the median fund starts looking bad and that’s where venture is right now.

The median 2021-vintage fund is tracking toward what might be a loss. The median fund across 2021-2023 is returning roughly what you'd get in a money market account, but with a 10-year lockup and zero liquidity. The math only worked when entry prices were low and exit multiples were high. Now entry prices are elevated and exits are constrained — and essentially no amount of portfolio construction optimization changes that fundamental equation.

Will it eventually cycle back? I don’t think so. Hedge fund returns didn't magically recover — the industry just shrank until the remaining capital could find enough alpha to justify itself. PE returns haven't gone back to the glory days of early 2000’s. And that’s probably the future of venture. Not dead — but harder.

Follow the Last Money In authors on LinkedIn