- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- 💡Venture Capital Should Not Be Democratized Unless...🎓

💡Venture Capital Should Not Be Democratized Unless...🎓

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

June 12, 2024

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

Fill out our unique form to get to the top of the line here.

Deal Sheet = top weekly VC SPV investment opportunities at 10% carry (instead of 20%).

This week we shared 5 deals from early-stage to growth stage across 4 different syndicate leads. Co-investors include Bessemer Venture Partners, a16z, Redpoint, Jason Calacanis, Scale Venture Partners among many others.

To get access to these deals at 10% carry you can sign up for Deal Sheet here or book a call to learn more!

💡Venture Capital Should Not Be Democratized Unless...🎓

As a venture capitalist who spends all his time sourcing, diligencing and raising capital from primarily retail accredited investors, I should be heavily incentivized to support policy that expands the venture capital asset class to a policy framework that includes more retail participation.

But I generally do not support asset class expansion unless there were extremely “smart policy” that expanded VC participation based on expertise and NOT on income, wealth, other financial and worth related benchmarks, etc.

The Prevalence of Startup Failures and Losses & Outsized Impact of Outlier Successes:

Venture capital involves investing in early-stage, extremely high-risk startup companies - if you don’t know what you’re doing it's one of the fastest ways to lose a lot of money. The failure rate for startups is extremely high, with most venture investments resulting in total losses; even firms like Andreesen Horowitz have publicly stated that the expectation is that half of their companies will go to zero. According to an Industry Ventures report; they cited “the work of our friend Trevor Kienzle’s firm, Correlation Ventures, which analyzed 21,000 financings for the period 2004-2013. They found that 64% of all VC investments lose money.”

What’s more interesting is that based on data that Industry Ventures put together, several of the funds with the highest MOIC (Multiple on Invested Capital - essentially shows how many multiples of the original investment amount have been generated) had very high loss ratios, e.g. a 2007 vintage, had a 4.4x MOIC (considered very good) and a 66% loss ratio.

Additionally, according to estimates from Holloway Guide to Raising Venture Capital, an estimated 4% of venture investments produce returns of 10x or more, and only 10% produce returns of 5x or more. This is all to underscore, even the best managers lose on capital on the majority of their investments, and the outlier (or outliers if you're so lucky) will drive almost all of the return.

I’ve seen this in my own syndicate (~8,000 LPs & ~500 SPVs completed) that even most accredited investors today don’t follow basic principles that can set themselves up for success or failure with the primary underlying principle being as a LP in SPVs you are the fund manager.

SPV LP’s - You are the Fund Manager:

Why is that so important - when you invest in a fund, there’s only a set amount of capital you can lose and you have someone optimizing portfolio construction and diversification for you (e.g. the fund manager), which in early stage venture capital is extremely important; again, missing the outlier is the difference between receiving 3-10x+ return on capital versus 0-1x capital back. When you invest in SPVs, you are exclusively responsible for portfolio construction (i.e. you are the fund manager…).

To give a real live example that is close to me: a GP friend of mine who has syndicated approx. 20 investments (+/-) will have most of his investments return <1x back, and one that is on a clear path to return 100x-500x to his LPs, and let me tell you, the company that ended up being the outlier was extremely non consensus at the pre-seed when he syndicated the investment.

As an LP, if you invested your allocated VC capital into only 8 of his 20 syndicated investments, odds are you missed the outlier (only 40% chance you invested in the outlier) and will likely make 1x capital back or less over a ten year period; a horrible return.

If you diversified your investments more and invested in all of his 20 startup opportunities (albeit less capital into each), you are on a very clear path to 5-20x+ your capital in a <10 year period. Some LPs are positioned to make $10M+ on relatively small checks (<$25k) if things continue on their trajectory (which I could be wrong but I think they will based on all of my knowledge on this company).

Unfortunately most of his LPs weren’t diversified enough and missed the outlier… this could have partially been avoided with education on optimizing portfolio construction.

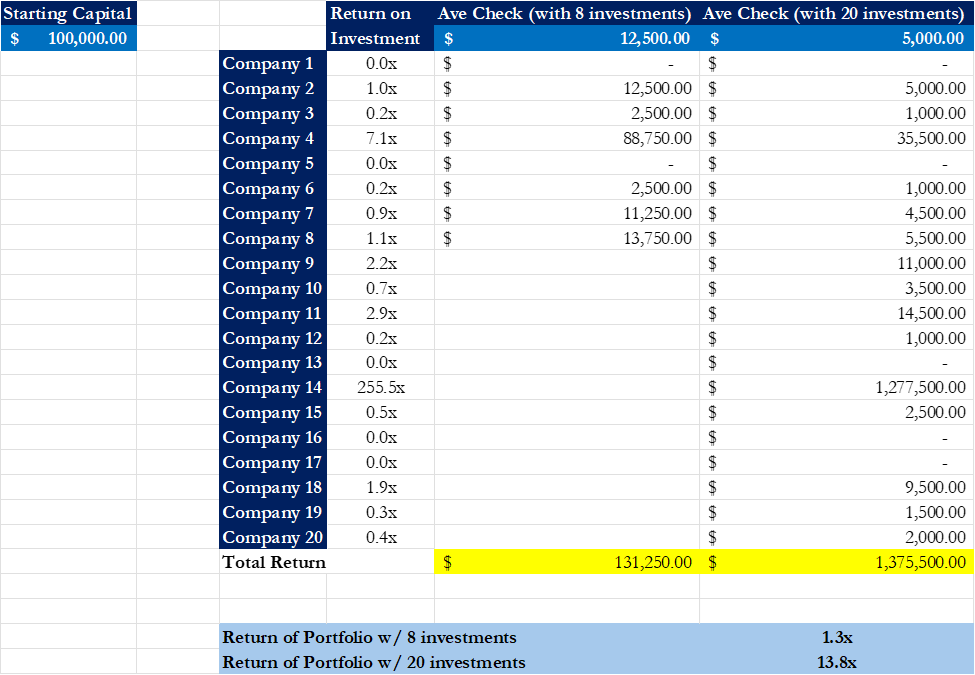

Here’s a basic example of this model at work:

Let’s assume I have $100,000 in capital to invest across 20 Seed opportunities I’ll see from a GP over the next 36 months. I’m considering 2 scenarios: Invest $12.5k into 8 of the most interesting syndicated opportunities ($100k total invested); Invest $5k into all 20 of the syndicated opportunities I see over the next 36 months (also $100k total invested). As it turns out, the majority of his Seed opportunities returned 0-1x capital back (consistent with Seed VC), but one of the 20 syndicated investments returned 255x on capital (e.g. the outlier).

Unfortunately because I only took 8 shots on goal, I missed the outlier in my 8 bet portfolio (I only had a 40% chance of hitting it (e.g. 8/20 = 40%)). On my second mock portfolio however, I hit the outlier as I had exposure to all 20 investments So while my second portfolio had a smaller average check size ($5k versus $12.5k for the more concentrated portfolio), my performance was massively better (13.8x return on capital versus 1.3x return).

While this example is tailored to me, it’s based on what I see all of the time - construct a portfolio that diversifies enough shots on goal, because missing the outlier is often the difference between 1x (or less capital back) and a great return. Think deeply about portfolio construction.

To be fair, if you’re concentrated portfolio of 8 bets hit the outlier, you would have 2-3xed more capital the fully diversified portfolio of 20 bets, but odds are you missed it with a concentrated portfolio, and this is consistent with many LPs in SPVs, who want to cherry pick and concentrate in what’s perceived as the best 5-15 Seed opportunities when in reality that’s a failed strategy for almost everyone. There’s a reason most Seed funds have a minimum 20-25 investments in their fund with some having upwards of 50 investements in a single fund.

And this brings me to the real topic of this article…

We Need to Rethink VC Accreditation with a Sophistication-Based Approach:

Unfortunately the lack of diversification and lack of exposure to the outlier specifically led to a lot of LPs in this GP’s SPVs missing out on life changing gains. And has led me to strongly believe that just because you’re rich doesn’t mean “you’re sophisticated” and shouldn’t qualify you to invest in startups, and the opposite is true as well (i.e. just because your not rich doesn’t mean your not sophisticated and should be excluded from participation in VC)…but that is what’s happening today and it’s stupid and BAD for the ecosystem.

What Policy Would I Support:

I support policy that re-writes the entire accreditation book to include only those that are sophisticated, and not “sophisticated” by current SEC standards (e.g. based on income, wealth primarily), but one that is based on what sophistication should mean (e.g. how well do you understand private markets investing).

In the same way I was required to take a number of “Series” exams to be an investment banker earlier in my career; we need sophistication exams to qualify retail as sophisticated to invest in the venture capital asset class.

Of note, I don’t envision these tests qualifying individuals for finance experts like a CFA but rather for an understanding of 1) basic principles in venture capital – e.g. structures, terms that are frequently discussed in books like Venture Deals, 2) qualifying for an understanding of the different ways to evaluate deals, 3) qualifying for basic understanding of principles in portfolio construction, and 4) ensuring that you can manager your own risk properly.

For brevity these are a few of the general principals.

Designing a VC Sophistication Exam

Here is a very basic category test template for qualifying investors for sophistication over current standards of wealth:

Section 1: Fundamentals of Venture Capital

Definition and role of venture capital in the startup ecosystem

Stages of startup funding (seed, series A, B, etc.)

Common investment structures (SAFEs, convertible notes, priced equity rounds)

Key terms and concepts (valuation, dilution, liquidation preferences, etc.)

Section 2: Evaluating Startups

Assessing founding team, market opportunity, product, traction, and competition

Understanding and interpreting startup financials and metrics

Identifying red flags and common pitfalls in startup investing

Due diligence best practices and resources

Section 3: Portfolio Construction and Risk Management

Importance of diversification in VC investing

Strategies for allocating capital across stages, sectors, and geographies

Understanding power law distributions and the impact of outliers

Managing liquidity and cash flow considerations in illiquid investments

Section 4: Legal and Regulatory Landscape

Overview of securities laws and regulations relevant to VC investing

Accreditation requirements and their implications

Key legal documents (term sheets, stock purchase agreements, investor rights agreements)

Tax considerations for VC investments

Section 5: Ethical Considerations and Fiduciary Duties

Identifying and managing conflicts of interest

Responsibilities and best practices for investor communication and reporting

Promoting diversity, equity, and inclusion in VC investing

Balancing financial returns with social and environmental impact

The exam could feature a mix of multiple-choice questions, case studies, and open-ended responses to assess both conceptual understanding and practical application. A minimum passing score should be required to demonstrate a basic understanding of the material.

We need a complete overhaul of accreditation rules, and to be honest if we do this right we actually expand that asset class to those who should qualify to invest in the asset class and in so, democratize it.

If you enjoyed this article, then check out our prior articles on LP support

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!