- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- The Challenges of Relying on Public Comparables for Valuing Your Startup

The Challenges of Relying on Public Comparables for Valuing Your Startup

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

January 08, 2025

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

The Challenges of Relying on Public Comparables for Valuing Your Startup

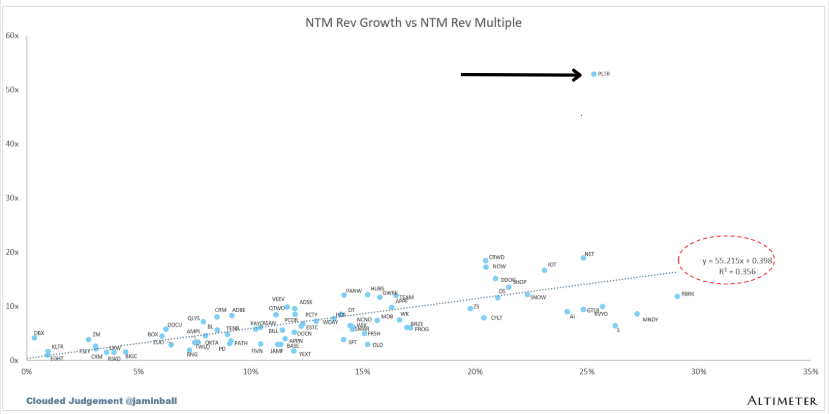

In a recent analysis from Altimeter's Clouded Judgement newsletter, a unique visualization emerged that captured my attention. The scatter plot, mapping Enterprise Value to Next Twelve Months (NTM) Revenue Multiple against NTM Revenue Growth, revealed Palantir as a statistical anomaly against the rest of the SaaS comp set.

While the broader SaaS landscape demonstrated a relatively consistent correlation between NTM growth and NTM revenue multiple, with companies generally commanding NTM revenue multiples at 20x or lower, Palantir stood as a complete anomaly, commanding a staggering 50x NTM revenue multiple, despite lower NTM growth rates than Monday and Rubrik.

Palantir: A Statistical Outlier in SaaS Valuations

The bullish narrative surrounding Palantir presents compelling evidence for the company's performance and potential. CEO Alex Karp's assertive statements about "unrelenting" AI-driven demand reflect the company's strategic positioning at the intersection of artificial intelligence and enterprise solutions. The company's Q2 2024 performance metrics are particularly noteworthy, with commercial revenue expanding by 33% globally and an impressive 55% growth in the U.S. market, demonstrating strong market penetration and growing enterprise adoption.

Some institutional investors have begun positioning Palantir alongside established Big Tech leaders, projecting a potential trajectory toward a trillion-dollar market capitalization. This ambitious outlook stems from the company's expanding Total Addressable Market (TAM), particularly as AI integration becomes increasingly critical across industries. The convergence of Palantir's government contracts, commercial expansion, and AI capabilities has created a unique value proposition that has captured market imagination.

However, this strong market positioning and performance, while impressive, should not be misconstrued as a broadly applicable valuation benchmark.

The danger lies in private defense technology companies using Palantir's 50x revenue multiple as justification for premium valuations for its private market counterparts. This approach is fundamentally flawed and that’s where we get into trouble as VCs.

💵 Last Money In Deals: We have made over 800 startup investments. Accredited investors & qualified purchasers within the LMI community can now gain access to our alternative investments such as venture, late-stage growth, and private equity through our deal flow sheet. Interested (it's completely free)? Fill out this form.

👜Try Deal Sheet for Free: Want to join hundreds of subscribers in trying Deal Sheet, our premium newsletter that provides you access to the top venture deals with discounted carry. Try Deal Sheet for free for 7 days here.

🐦 Follow Us: Visit Alex’s Linkedin and Zach’s X account for constant updates on all things venture capital, SPVs and more!

Historical Cautionary Tales

The market's current enthusiasm for defense and AI focused companies, while justified in cases of proven capability and scale, should not be interpreted as a blanket justification for premium multiples across the defense technology sector. Each company's valuation should reflect its specific business fundamentals, market position, and growth trajectory, rather than drawing direct comparisons to statistical outliers like Palantir today.

The evolution of public market valuations has shown that certain companies can sustain premium valuations when they create or dominate new categories and sometimes justifiably so, but oftentimes probably not!

It was only three years ago that Peloton hit a $50B market cap during the height of the stay at home boom, leading to a FLOOD of overvalued home gym equipment startups like Hydrow, Mirror and many others getting valued at extremely premium valuations based on public comps like Peloton at the time. For context, Peloton is valued at only ~$3B today despite improving its net income, among other metrics over the period. Peloton’s multiple at the time was massively out of historical norm.

Similarly it was only three years ago that Beyond Meat reached a $10B valuation with what seemed like a certainty that plant based meats and foods were the future of health and sustainability. And with that Impossible Foods, Meati, and so many other plant based meat private startups reached sky high valuations on this comp that have sobered dramatically since that trend has dwindled away with Beyond Meat valued today at just $260M. That’s a 97% drawdown, mostly due to mass multiple compression.

Or take fintech 2021. Affirm reached a ~$60B valuation and >50x revenue multiple, which led to a highly expensive and premium multiple for Afterpay (from Square) and a whole slew of fintech startups receiving similarly exorbitant multiples. Affirm’s revenue multiple has since compressed by over 80%, as has its fintech counterparts…

There are other examples that date long ago such as Cisco in 2000, which established itself as the market leader in routers and switches, critical components for internet infrastructure and led to a boom of comps in this space getting far too overvalued. The industry grossly overestimated the immediate demand for bandwidth. While internet usage was growing rapidly, it didn't match the astronomical projections that drove massive infrastructure investments. Cisco still hasn’t reached its dot com valuation peak 25 years later, nor have many of its comps at the time like Juniper.

These extreme, but often occurring, historical examples suggest that while outlier valuations can persist, they often normalize as markets mature and competition increases, and it's important to keep this in mind when comping your hot private startup that’s operating in one of these categories or companies.

So please take caution when using these outlier comps when investing in private market comps!

Key Lessons from Market Anomalies

When exceptional valuations emerge in the market, they offer valuable insights for investors. First and foremost, context is everything – we need to dig deep into the forces shaping these outliers, from interest rate environments to broader economic conditions, before judging whether such multiples make sense.

It's also worth remembering that what looks like a "new normal" in markets often proves temporary. Today's seemingly revolutionary trend might be tomorrow's cautionary tale. And while it's tempting to anchor to prominent examples, putting too much weight on a single comparison can lead us astray.

This becomes particularly crucial in private markets. Unlike public market traders who can quickly exit positions, private market investors are typically locked in for years. The stakes are simply too high to rely on cherry-picked comparisons without thorough analysis.

So how can investors develop more reliable valuations?

Start by casting a wider net – look beyond the obvious comparisons to build a more comprehensive view. Ground your analysis in business fundamentals rather than just market multiples. Think through multiple scenarios, both optimistic and pessimistic, to stress-test your assumptions. And perhaps most importantly, question whether today's market enthusiasm can truly sustain itself over the long haul.

Of course it's worth mentioning cases where the hype was real and it was worth it to pay a premium in the private markets to invest.

Take Social Media in 2005-2012. During the rise of social media platforms, valuations for companies like Facebook, Twitter, and LinkedIn were considered extremely high by traditional metrics. For example: Facebook's $15 billion valuation in 2007 (when Microsoft invested $240 million for a 1.6% stake) was seen as astronomical for a company with only $153 million in revenue. Twitter's $1 billion valuation in 2009, when it had virtually no revenue, was criticized as excessive.

However, these valuations proved to be justified: Facebook went public in 2012 at a $104 billion valuation and is now worth over $1 trillion. Twitter went public in 2013 at a $31 billion valuation and was acquired by Elon Musk for $44 billion in 2022. LinkedIn was acquired by Microsoft for $26.2 billion in 2016, a significant premium to its IPO valuation - today a price that was clearly a steal by Microsoft.

I’m mentioning this to underscore that the point of this article isn’t to disregard massive trends entirely (and the premium comps that pop up as a result), but to take a sober, balanced framework during your comps eval. especially when outliers, like Palantir, in today’s market persist.

Conclusion: Finding Balance in Valuation Analysis

While history shows us that some hype cycles - like the early social media wave - produced valuations that were ultimately justified by fundamental business success, others - like the recent plant-based meat phenomenon or Cisco in the early 2000’s - proved to be transitory bubbles that left many investors underwater and that in hindsight, shouldn’t be used to comp the sector...

The key lesson from examining these cycles is not that high multiples or outlier valuations are inherently flawed, but rather that thorough diligence and contextual analysis remain perhaps more crucial. When faced with a Palantir-like outlier in public markets today, investors must resist the temptation to apply blanket comparisons to private market valuations. Instead, success lies in doing the fundamental work: understanding company-specific drivers, evaluating sustainable competitive advantages, and analyzing both macro trends and micro execution capabilities.

In the end, while public market comparables provide useful reference points, they should serve as just one data point in a comprehensive valuation framework, not as a shortcut to justifying premium valuations in private markets.

If you enjoyed this article, feel free to view our prior articles on adjacent topics

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!