- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- 📈 5 Traits of a 15x+ Revenue Multiple Business

📈 5 Traits of a 15x+ Revenue Multiple Business

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

May 29, 2024

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

Fill out our unique form to get to the top of the line here.

5 Deal Sheet deals, across 5 different syndicate leads shared on Monday

This week we shared 5 deals across 5 different syndicate leads (via Deal Sheet), a true curation of SPV’s for some of the ecosystems top Syndicate/SPV leads! Deals included:

Series A Biosciences company

Pre-seed for a new co led by a founder who took his last company to > $40m run rate

One of the world's longest-standing digital asset platform (Special 0% carry on this one)

Fast moving Nuclear Power Company raising series A

Pre-Seed Innovative Robotics company

Deal Sheet is our paid offering that provides accredited investors top weekly venture capital SPV investment opportunities and at discounted carry.

You can sign up for Deal Sheet here or book a call to learn more!

📈 5 Traits of a 15x+ Revenue Multiple Business

Investors highly value software-as-a-service (SaaS) companies that can achieve and sustain rapid revenue growth while also demonstrating strong profitability and cash flow generation. In the public and private markets, a select group of SaaS businesses are commanding premium revenue multiples of 15 times LTM (last 12 months) or higher.

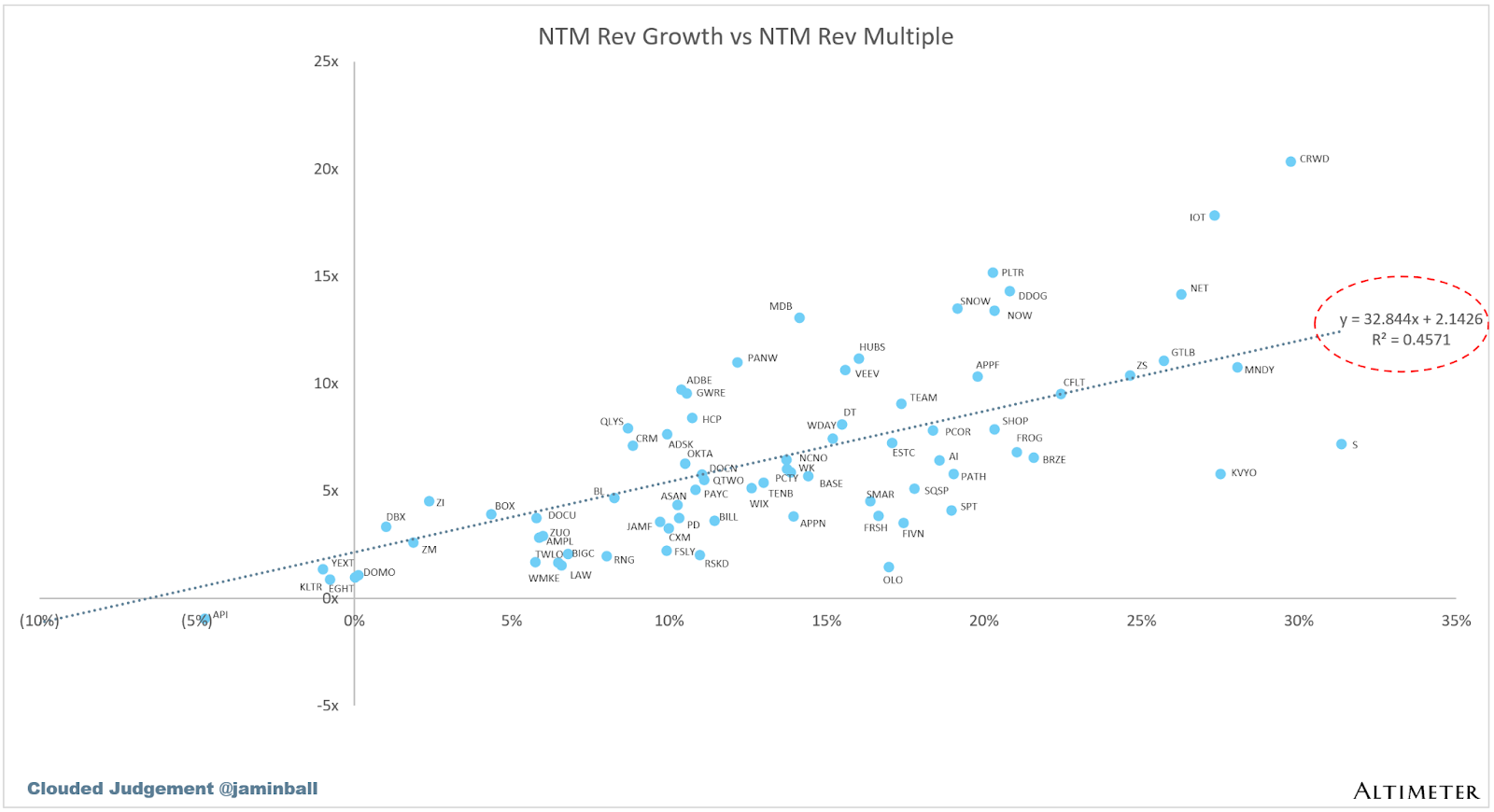

According to Clouded Judgment (Altimeter’s SaaS newsletter), there are approximately seven public SaaS companies that are trading at 15x+ LTM Revenues within a dataset of 80+ public SaaS companies; they are Cloudflare, Crowdstrike, Palantir, Datadog, Samsara, Snowflake, and ServiceNow.

Understanding the key traits that distinguish these highly valued 15x+ LTM Revenue companies is crucial for both entrepreneurs, VCs and investors all around. Today, we’re exploring the critical factors that drive such high valuation multiples, including digging deeper on the higher correlated inputs such as revenue growth, profitability + free cash flow generation, and widely adopted measurements such as the "Rule of 40" metric.

By beginning to dissect the characteristics / KPIs of these high multiple SaaS players, we can gain some insights that can help drive your own analysis of private/public software companies.

So what metrics do you need to justify a 15x+ revenue multiple?

Revenue Growth

Unsurprisingly, companies with a consistently high revenue growth rate, especially in large addressable markets, tend to command higher revenue multiples. Investors are willing to pay a premium for companies that can sustain rapid top-line growth over an extended period with correlation coefficients between revenue growth rates and revenue multiples trending in the range of 0.7 to 0.9 (or higher) for SaaS companies, indicating a very high degree of correlation.

Notably, every single aforementioned SaaS company that presented EV/LTM revenues of >15x today has an LTM revenue growth of over 20% except one, while the Median LTM growth rate of all of the 80+ SaaS companies listed was only 17%.

The same is true for NTM (next 12 months) growth with all but one company in the 15x+ LTM Revenues category having a NTM growth rate of 20% or more, while the median for all 80+ listed SaaS companies was only 13%.

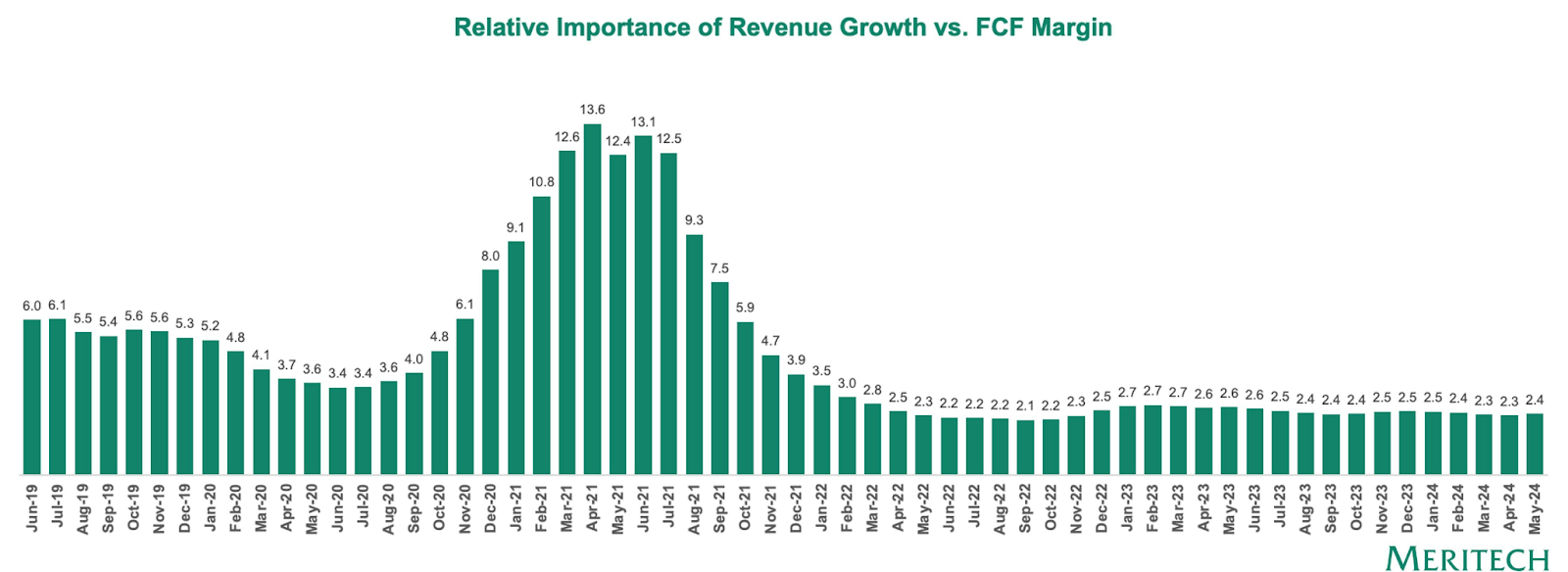

Additionally, according to a May 2024 Meritech's analysis report, growth is 2.4x as correlated with multiple vs. FCF margin. Said another way, a 1% increase in growth would have the same impact on multiple as a 2.4% increase in FCF margin.

According to the report this is down substantially from the 2021 period, where the relative importance of revenue growth vs. free cash flow (FCF) margin reached a peak of 13.6 but nonetheless underscores the relative importance of growth > profitability in spite of increased emphasis on business model, margin and FCF today versus the 2021 period.

The median revenue multiple for the top 10% of SaaS companies has fallen 60%+ from its 2021 peak, and still below pre-COVID levels, highlighting the continued premium placed on high growth despite substantial multiple compression.

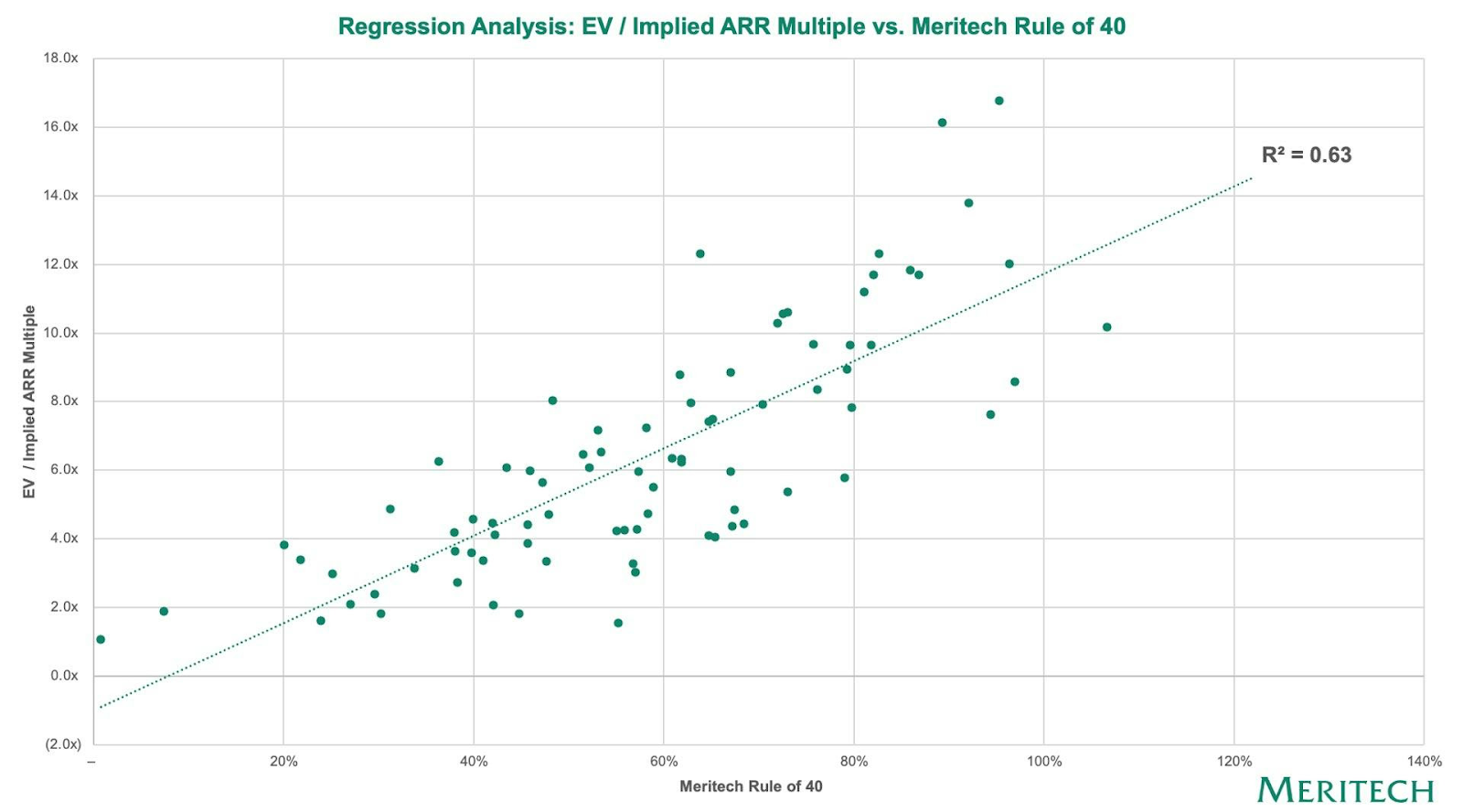

A widely used benchmark for software and subscription-based companies, the "Rule of 40" metric (FCF + Revenue Growth), which weights growth multiples more than profitability, shows a stronger correlation to valuation multiples than just growth or profitability alone. According to Meritech data, “...companies with similar Rule of 40 but growing faster can trade at a significant premium (8.6x) to companies with lower growth and higher free cash flow margins (4.6x)....Investors pay the highest prices for companies that are growing quickly and have some free cash flow.”

And this correlation isn’t a new trend.

We went back to the earlier days of SaaS in 2013, and even then saw extremely high correlation between multiples and revenue growth.

According to a 2013 (yes 2013..) report from Dave Kellog (at Balderton Capital at the time) titled “What Drives SaaS Company Valuation? Growth!” he found that as a rule of thumb that "Basically (growth rate % / 10) + 1 = forward revenue multiple; so a 10% growth rate would equate to a 2x revenue multiple, 20% growth to 3x, 30% growth to 4x, and 50% growth to nearly 6x, and so on.” In other words, revenue growth as an extremely high correlator of SaaS multiples isn’t anything new.

Free Cash Flow (FCF) Margin

FCF is the cash a company generates from operations after accounting for capital expenditures and changes in working capital. Companies with high FCF Margins (e.g., above 20-25%) are generally valued more highly as they have greater financial flexibility and can reinvest in growth initiatives.

High revenue growth alone is not always enough to justify a premium multiple and that is never more obvious than today after seeing cash burning unicorns end up coming bust in spades. Investors are increasingly looking for companies that can efficiently convert that revenue into cash flow. Companies with strong FCF generation demonstrate financial discipline, operational efficiency, and the ability to self-fund growth initiatives. Robust FCF allows companies to reinvest in research and development, make strategic acquisitions, or pursue other growth opportunities without relying heavily on external financing.

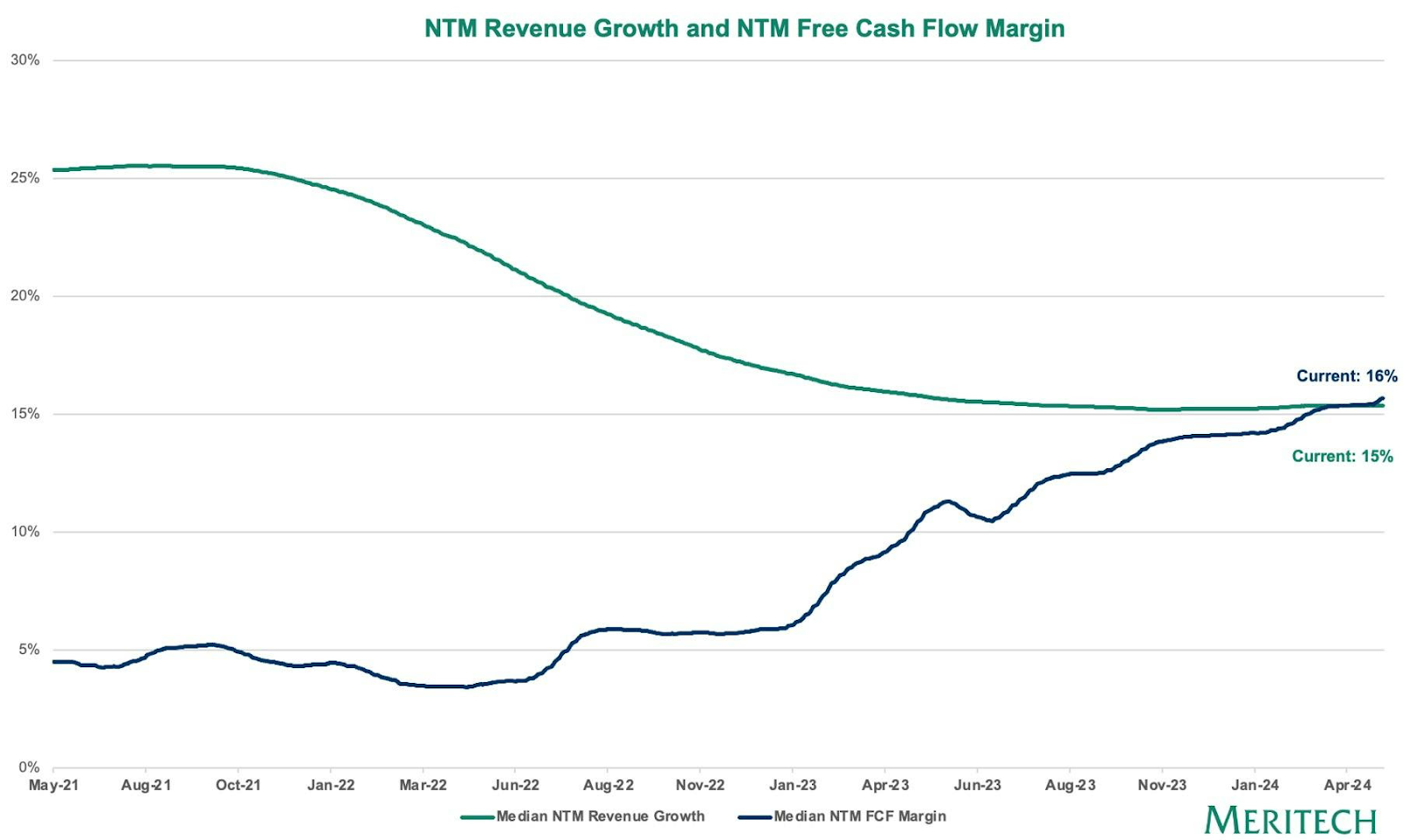

“Public SaaS companies have rapidly shifted towards efficiency. Forward growth rates have come down dramatically, and free cash flow margins have risen across the board. Put simply, companies are trading growth for profitability in today’s market.” - Meritech

And according to Altimeter data, the top ten most highly valued EV/LTM Revenue multiple companies all have positive FCF margin except one with the Median of the companies at >15x LTM Revenues at 25%+ FCF versus 13% for the entire cohort of SaaS companies.

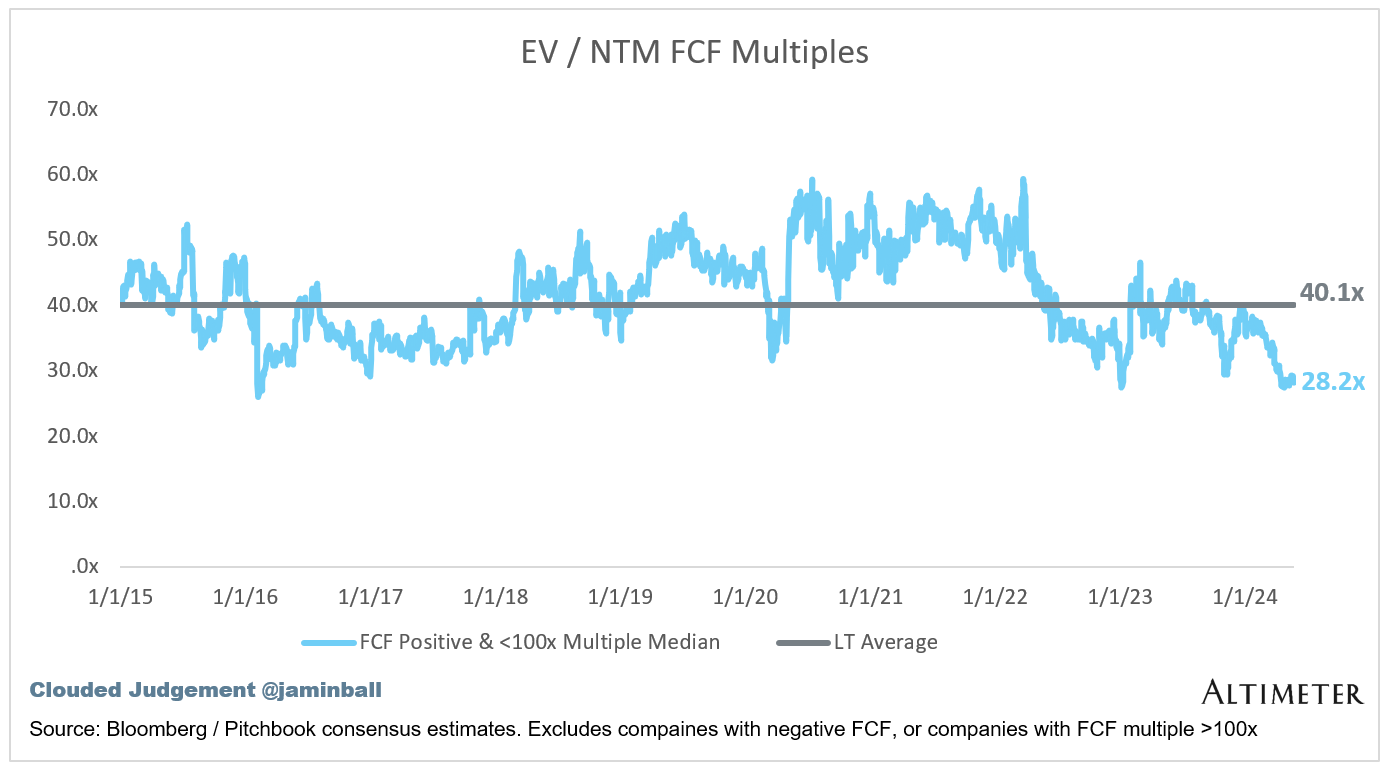

As mentioned, regression analysis from Meritech showed that a 1% increase in revenue growth has the same impact on valuation as a 2.4% increase in FCF margin. However, the Enterprise Value to FCF (EV/FCF) ratio is one common way to assess company valuations (but with limitations) with it being a highly valued correlating factor to overall valuation.

Interestingly, as shown by Altimeter’s Jamin Ball, FCF multiples have hit 10 year lows (tied with Covid lows and early 2016 lows). This isn’t necessarily indicative that FCF is less correlated, but more that valuations overall are lower, which isn’t that surprising given the 10Y is higher than it’s been in the last 10 years, so it makes sense multiples are lower.

Rule of 40

The Rule of 40 is a widely used benchmark for software and subscription-based companies. It suggests that a company's revenue growth rate (%) and profit margin (%) should add up to 40% or more.

For example, a company with 30% revenue growth and 20% profit margin would meet the Rule of 40. A company with 70% revenue growth and negative 50% profit margins would not meet the Rule of 40. Companies that exceed the Rule of 40 are often valued at higher revenue multiples.

To illustrate our point, Meritech established that growth has (today and historically) an outsized influence on software company valuations relative to FCF margins. So, rather than plot regressions of growth and Rule of 40 separately, Meritech plotted multiples against an adjusted Rule of 40 score, where growth receives a disproportionate weighting (in this case, 3x) relative to FCF margins – the Meritech Rule of 40. This metric more accurately reflects the valuation environment as shown in the prior chart and results in a higher correlation.

Every single company in Altimeter’s set of SaaS companies at 15x+ LTM/Revenues beats the rule of 40 (i.e. all are above 40%).

A study by Bain & Company found that software companies outperforming the Rule of 40 had valuations double that of companies below the 40% threshold. They also achieved returns 15% higher than the S&P 500.

Rule of 40 has become an important benchmark in the SaaS world because it captures the ideal equilibrium between scaling the business rapidly and operating profitably - two key drivers of long-term value creation.

FCF Growth

While FCF yield (current FCF divided by market value) is an important metric, FCF growth may be an even more important driver of valuation. FCF growth rates consistently above 20% annually are considered impressive and indicative of a company's ability to compound cash flows. FCF growth is often a better indicator of a company's future growth potential than just looking at earnings growth, as these companies are more likely to be able to invest in and expand their business, gaining a competitive advantage.

Additionally, to perform a discounted cash flow valuation (DCF), a financial analysis method used to estimate the value of an investment or a company by discounting its expected future cash flows to their present value, you’ll need to forecast the FCF of the company for a certain period, usually 5-10 years.

DCF models are extremely sensitive to FCF growth; even a 1% change in the FCF growth rate can lead to a substantial change in the company's implied valuation. FCF (and Terminal Value, which uses FCF as an input) are considered to be the more sensitive parts of the DCF model.

According to a report by Brown Advisory, for high-growth companies, even a 1% change in the long-term FCF growth rate assumption can move the valuation by 10-20% or more. As mentioned, this is partially because valuations are highly sensitive to terminal value calculations which rely heavily on the perpetual growth rate.

The impact is amplified for companies with higher valuations or lower current FCF yields, while for mature, low-growth companies, a 1% change in growth has less impact since terminal value makes up a smaller portion of the valuation.

Quality of Revenues

Quality of revenues refers to the sustainability, consistency, and other characteristics of a company's revenue streams. Its really referencing factors beyond just the top-line revenue number to assess the underlying strength and reliability of the revenues.

As an example, is $1m of one time revenue with negative gross margins equally valuable as $1m of recurring, sticky revenue with high margins and that can expand over time via upsells (i.e. Gross + Net Revenue Retention)? Of course not.

We put together a whole article that references between high quality revenues and low quality revenues which you can view for a deeper reading on this topic via Why Revenue ≠ Revenue! How to See Past the Blanket Revenue Multiples Put on Companies, but in general higher quality revenues are generally viewed more favorably by investors and analysts.

Here are some key aspects that define the quality of revenues:

Recurring vs. One-time: Recurring revenues from subscriptions, long-term contracts, or consumable products are considered higher quality than one-time or irregular revenues.

Visibility and predictability: Revenues that are highly visible and predictable based on backlog, customer relationships, or market positioning are viewed as higher quality.

Diversification: A diversified revenue base across multiple products, services, customers, or geographies is generally considered higher quality than a concentrated revenue stream.

Pricing power: The ability to raise prices without significantly impacting demand is a sign of higher quality revenues and pricing power.

Customer stickiness: Revenues from customers with high switching costs or strong loyalty are typically viewed as higher quality.

Margins: Higher gross margins and operating margins generally indicate higher quality revenues as they suggest pricing power and efficient operations.

Growth sustainability: Revenues growing organically from existing operations are often considered higher quality than inorganic growth from acquisitions or low-quality sources.

And so on.

Take Crowdstrike – it has high Gross Margin (75%), high FCF producing (31% LTM), high expansion revenue (119% NRR) with a relatively low payback among other factors, and in turn has been rewarded with a 20x+ LTM revenue multiple. Conversely, Domo is yielding a 1x revenue multiple, partially based on the quality of its revenues - it has negative FCF margin, 91% NRR (customers are spending less year over year), and an extremely high payback, among other difficult business metrics and characteristics.

Not all revenue is created equal.

We’re just scratching the surface on this topic, but in short, main factors driving high valuation multiples are revenue growth, free cash flow (FCF) margin, adherence to the Rule of 40, FCF growth, and the quality of revenues. We’re releasing a part two that will go into other highly correlative factors such as competitive advantage, scalability and operating leverage, market tam and potential, expansion/retention, etc. Stay tuned as we dive deeper into this topic.

If you liked this topic or any of our topics, please share on social or forward to someone who would be interested - it goes a long way!

If you enjoyed this article, feel free to view our prior articles on valuation and analysis:

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!