- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- Bridge Rounds; A VC’s Dream or Nightmare?

Bridge Rounds; A VC’s Dream or Nightmare?

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

February 08, 2025

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

Deal Sheet Free Trial. Start your 7 day trial here!

Deal Sheet provides accredited investors:

Access to some of the best startup opportunities across the VC syndicate ecosystem (est. 150-200 deals on Deal Sheet per year) and

All Deal Sheet deals come at discounted carry – all opportunities on Deal Sheet are listed at 10% carry (versus 20% standard) with select opportunities (at our discretion) at 0% carry.

Try the free trial today here!

Bridge Rounds; A VC’s Dream or Nightmare?

I sent out a post to my LPs in 2022 about my affinity for strong bridge financings. Another GP had put out a post warning of these rounds, and given our success (and luck) finding interesting bridge financings, we felt compelled to launch a post discussing how we view bridge rounds (different types, what we like, dislike, etc.).

The 2022 rant read:

“I saw another GP post about bridge rounds and thought I’d chime in with some quick commentary as I’ve thought about this quite a bit.

There are generally 3 types of bridge rounds

Bucket #1 - Company’s performing well but not well enough to justify a larger priced round and/or at their target valuation. In this current market where multiples have compressed 50-80%, this is happening more frequently.

Bucket #2 - Company underperformed for some semi-legitimate reason (supply chain issue, capacity issue, product bug, R&D required more time than expected, revenue lagging traction, etc.), but you build conviction that this is a temporary hitch with the original investment thesis more or less intact, though likely with some added runway risk or other risk.

Bucket #3 - Company’s underperforming, and the round is one last ditch effort to make something happen i.e., a bridge to death.

I’ve seen them all many dozens of times. #1 and #3 are generally (but definitely not always) easy to spot - #2 is tricky.

💵 Last Money In Deals: We have made over 800 startup investments. Accredited investors & qualified purchasers within the LMI community can now gain access to our alternative investments such as venture, late-stage growth, and private equity through our deal flow sheet. Interested (it's completely free)? Fill out this form.

👜Try Deal Sheet for Free: Want to join hundreds of subscribers in trying Deal Sheet, our premium newsletter that provides you access to the top venture deals with discounted carry. Try Deal Sheet for free for 7 days here.

🐦 Follow Us: Visit Alex’s Linkedin and Zach’s X account for constant updates on all things venture capital, SPVs and more!

My view is that if I can get in a bridge round that falls into the 1st bucket – the company’s performing well, but requires additional runway to hit the benchmarks required to raise a larger, priced round at a sufficient markup – I typically take it. It’s one of the few times for LPs to get significant value in a high performing company in venture, and these rounds have been some of our best performing deals. Without disclosing names, here are a few that come to mind:

Series A bridge for a B2B SaaS co at a ~$35M pre-money valuation that subsequently raised multiple large, priced rounds, the last taking place at an $800M+ valuation from lead Insight Partners. At the time, it was pretty clear this company fell into the first bucket [today, the company is valued at >$1 billion]

Series A bridge for a consumer tech company at a $95M pre-money valuation; raised multiple subsequent priced rounds, the most recent one valuing the company at $1B+ from lead Goldman Sachs. The company pretty clearly fell into the first bucket [today, the company is lagging]

Series A bridge for a consumer tech company at a $20m cap; less than 12 months later raised at a $140M valuation from Andreessen Horowitz. It was not clear if this company would succeed and definitely fell into the #2 bucket – in this case, COVID was the reason for underperformance, and while there was significantly more risk, we felt that if they could manage through it, they could quickly raise at a substantial (3-5x+ markup), which they did. [today, the company continues to perform]

Seed bridge for an autonomous tech company at a $20M pre-money valuation. Acquired 1 year later for $250M.

Why would a high performing company offer investors value in a bridge? One common reason is because the company is just looking for a small amount of capital and to close quickly so that it can continue to execute. They’re less concerned with the small dilution hit, and thinking of the bigger picture, and will very likely more than make up for it the next round when they actually raise a significant amount of capital….”

Days after our post, a major fund admin conducted a data-driven analysis of bridge round investments on their platform, challenging the conventional venture capital wisdom that bridge rounds typically underperform due to adverse selection. After analyzing over 10,000 SPV investments, they discovered that certain bridge round deals actually ranked among their platform's top performers. Between 2018 and 2021, bridge rounds accounted for 25% of SPV investments on their platform, with seed round bridges comprising 30% of all bridge deals. The frequency of bridge deals showed a declining pattern as companies moved into later financing stages.

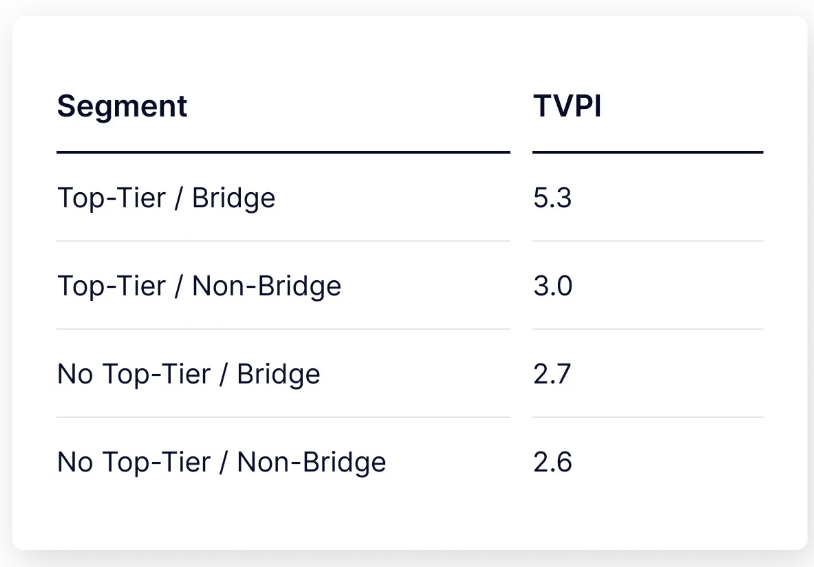

The analysis revealed that bridge rounds were most prevalent among early-stage startups, where founders often used them to extend their runway for user growth or product development. In contrast, later-stage startups seeking bridge financing were typically viewed less favorably by investors, as the need for additional funding could indicate fundamental business challenges. When examining deals involving top-tier VCs, approximately 15% were bridge rounds, with a similar pattern of decreasing frequency in later stages.

The study found that bridge deals with top-tier VCs generally showed declining performance in later stages. However, a deeper analysis revealed a surprising insight: on an indexed basis, bridge deals involving top-tier VCs emerged as the best-performing segment. For investments made after 2018 and aged 2+ years, the gross TVPI (Total Value to Paid-In capital) of bridge deals with top-tier VCs significantly outperformed other segments. This exemplified the power law of venture returns, where a small number of investments drive portfolio performance. Notably, these superior returns weren't attributed to a single outlier but rather to multiple strong performers within the segment.

Interestingly since this post, now over 2 years old, our view on bridge rounds still hasn't changed much from the above.

We still believe that bridge rounds can offer some of the best value in the venture market because valuations may be deprioritized to get quick closings. Because bridges are small by nature, the dilution hit isn’t usually terrible, which makes under pricing tenable.

Similarly we believe they can be trap rounds and a “bridge to death,” - in these circumstances, not only are rounds usually well overpriced as founders try to justify their last round or similar pricing (likely) when the company has likely very underperformed, but you're probably funding a last ditch effort that has an outsized probability of falling.

Sometimes bridge rounds are done for fantastic companies but you're not getting any value in the deal - as a syndicate, we’ll candidly take those to get our foot into the deal and build the relationship to hopefully continue to pile in more capital into future rounds.

As we look ahead through 2025 and beyond, these bridge rounds continue to represent both significant opportunity and notable risk. The key to success lies not just in pattern matching or rigid categorization, but in developing a nuanced understanding of company fundamentals, market dynamics, and the true motivations and fundamentals behind the bridge. The best investors have learned to differentiate between bridges built from strength (strategic runway extensions) versus bridges built from weakness (survival attempts).

While our early thesis about the potential value in great bridge rounds has largely held true, we've also gained a deeper appreciation for the importance of structured terms, insider knowledge, and market timing in these decisions. For funds willing to do the work, these rounds can continue to offer some of the most asymmetric return profiles in venture and we’ll continue to syndicate what we feel are the best ones.

If you enjoyed this article, feel free to view our other articles on adjacent topics

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!