- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- 5 Syndicate Learnings after Completing 500 SPVs (Part 2)

5 Syndicate Learnings after Completing 500 SPVs (Part 2)

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

July 24, 2024

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

Fill out our unique form to get to the top of the line here.

Deal Sheet: (pricing going up again) – Save Carry + Get Access

Deal Sheet our paid email offering that provides accredited investors:

Access to some of the best startup opportunities across the VC syndicate ecosystem (est. 150-200 deals on Deal Sheet per year) and

All Deal Sheet deals come at discounted carry – all opportunities on Deal Sheet are listed at 10% carry (versus 20% standard) with select opportunities (at our discretion) at 0% carry.

Pricing is going up again Thursday August 1st.

To date - Deal Sheet subscribers have received 0% carry opportunities (versus standard 20% carry) in a large number of highly prolific companies and 10% carry on almost 100 of the most interesting startup opportunities YTD from pre-seed to pre-IPO from across the syndicate ecosystem already this year. And this, for the price of just $3.5k/year →→→ Learn more here!

5 Syndicate Learnings after Completing 500 SPVs (Part 2)

We just closed and wired our 500th SPV at Calm Ventures; this is perhaps more than any single GP entity globally (albeit we get a lot of help from external partners, VCs, etc.). A few weeks ago we discussed five of our top learnings after completing 500 SPVs. Those included:

In SPVs, GPs are Not a Fund Manager

The GP Carry Economics are Really Superior

This Ecosystem is Highly Cyclical

There are A Lot of GP Hacks to Scale Quickly

SPVs are a Way to Move Fast, But Not a Way to Scale

Part 1 of this article is here for reference.

For part 2, we are going to dive into 5 additional major learnings from our experience over the last five years of putting SPVs together with now ~500 SPVs completed.

Let’s get into it.

1. Figure out your sourcing game

Notably Alex & I have very different sourcing models as do different funds. Funds like Summit are notorious cold calling machines to find great deals. Some funds like Proof built their model as a co-investment / pro-rata fund and work with VC funds directly to source the best opportunities. Another fund I’m close with leverages their deep technical network founders to get introductions into the companies on the bleeding edge of tech. Our sourcing is almost entirely done through partners including other syndicates and VCs; Alex sources primarily through relationships.

Point being there is not one size fits all for sourcing.

Notably your sourcing may evolve over time. I hesitated initially on starting my own venture firm because candidly I didn’t understand how to source. At my prior fund that I worked for, my sourcing was built primarily around a lot of cold emailing. When I started Calm that was my primary avenue for deal flow as well - unapologetically emailing any company that looked interesting and filtering/diligencing from there. It worked and we got some extremely strong access through cold and warm introductions. But the model evolved, quite organically, with now our sourcing done primarily through ongoing partners.

How did it evolve to this? Well it turns out that there are a lot of network effects built into this ecosystem. The more you’re involved in finding and executing investments, the more people you meet, the large reputation you get, the more people that want to work with you and so on. And that’s more or less how we shifted to a network driven firm.

In general I’d play to your strengths when it comes to sourcing deal flow. Do you have deep talent networks - if so leverage those. Are you a sales / hustling machine, then perhaps cold/warm introductions are your best bet. Do you have extreme value add - find the best companies that need your skills to win deals. Do you have a media presence and public brand - leverage it to build PR for founders you invest in. Whatever your strength and value adds are - play to them. Alex previously put out an article discussing different models of sourcing for viewing here.

2. Own the relationship with your LP

I got my start leveraging other syndicators distribution to build our LP base. The strategy worked well at the time and even still somewhat today, but you need to be building close relationships with LPs that you own (e.g. not just one’s that are discovering you via a marketplace model or via another GP’s distribution). This is one of the benefits of running SPVs on Sydecar - your LPs are your LPs and not discoverable.

I know syndicators that operate in complete silo and don’t take advantage of marketplace features (as we have traditionally done) to find LPs, and from my conversations with them, I find that they have a different level of loyalty and participation from their LPs. They can, in general, count on many of them to invest in their deals when they’re syndicating an opportunity because of the trust that has been established.

In an up market such as 2021, this loyalty didn’t matter as access to capital was extremely easy and loyalty among LPs didn’t matter as there was plenty of capital to go around. In a down market such as 2023/2024, this loyalty is likely paying dividends in the form of being able to consistently fill allocations for GPs that have been in the work.

My recommendation to anyone starting is irrespective of your approach, build lasting LP relationships.

3. Venture Capital is a decade long game - get creative with fees

The timeline to liquidity for a startup has gone from 5-8 years to 10-14 years for many of the best companies with some companies now staying private for over 20 years (e.g. SpaceX was founded in 2002 and is still private 22 years later).

If you’re running a fund, you’ll collect management fees and draw a salary. If you don't and are operating exclusively as a Syndicate GP then either you need to 1) charge fees on some of your SPVs or 2) get creative with how you’ll pay yourself.

My advice is to start by charging some management, even if it's small. That income will go a long way to float you, while you wait for venture outcomes. Alternatively, you can consult for startups (e.g. offer advisory services to help them with their pitch decks, financial models, sales process - whatever your strength is), generate side hustles (e.g. Last Money In / Deal Sheet have been highly profitable for Alex/I), do SPVs part time, while you maintain a full time job until you start making meaningful income, or other. Of note, Alex has been syndicating deals while at a previous startup and after that acquisition he helped launch Hampton, Sam Parr’s private founder community and did a consulting gig, so he has really managed to make money in other areas to support playing the long game as a syndicate lead.

For additional reading, we previously put together a whole article discussing whether SPV leads should take management fees; and what GPs do on the side to generate additional income if they do not. But in short - it takes a long time to get rich in venture (if ever), so have a plan to generate income while you await hopefully large carry checks down the line.

4. What is your thesis to make money in venture capital

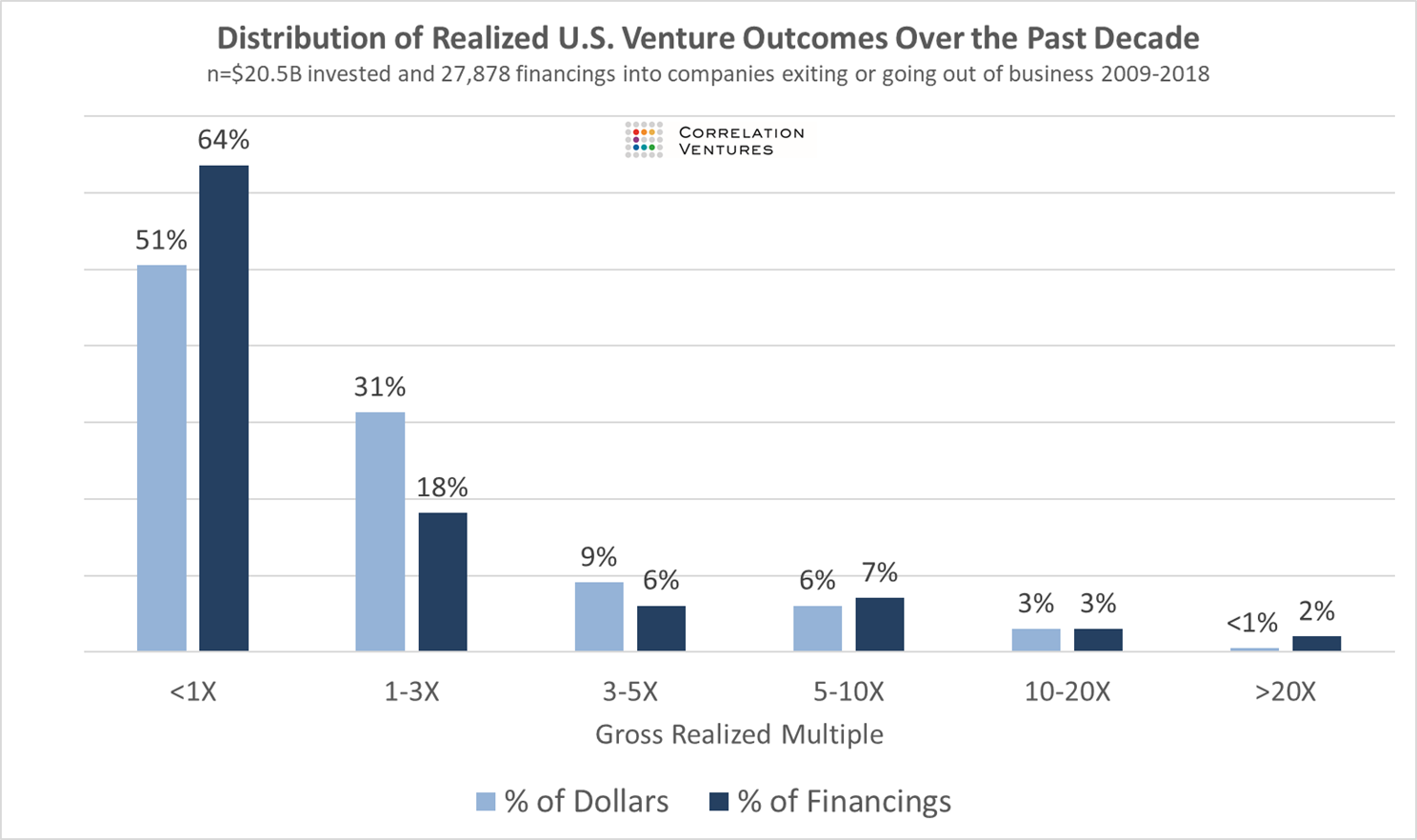

Venture capital is actually a very hard business to make money in despite the success stories. While venture historically has had some of the best returns of any major asset class, it’s also highly distributed with the top performing funds taking most of those gains. Around half of venture funds don’t even return 1x capital back, while the outliers can return 10-20x+ on their funds.

What this means for you is that you need a strategy to succeed. As a syndicate GP, you don’t need to think deeply on portfolio construction as you don’t have a limited pool of capital, but you do need think about what deals are most likely to make you money. It is very hard to get rich scathing together $100k SPV commitments into Series C companies - if you’re able to 5x (arguably a solid outcome), then you’ll only make around $80k in carry. Yeah it’s income, but it won’t generate real wealth.

One of our strategies today is to try to acquire as much ownership as early as possible. A $200k investment into a $5M company gives me 4% ownership in the business; even if I take no pro-rata I may turn that into a $30M distribution check in a multiple billion dollar outcome or a ~$6M carry check to the GP at exit. A $200k investment into a Series C company at best is likely a $1-2M distribution outcome in the best case or a $200k-$400k carry check to the GP at exit. It’s extremely important to think deeply about this - how will you make money in SPVs…

5. Reputation, reputation, reputation

You build a reputation over time and not just with LPs, but with GPs. There are GPs I won’t ever work with because they’ve shown themselves to be unethical, hostile, uninformed or other. Similarly, there are GPs that I latch onto and collaborate with extremely often because they’ve shown themselves to be trustworthy, easy to work with, have great deal flow, etc. Alex was one of those GPs and now we started a business together.

On the LP side, this is also the case. There is a syndicate out there with 10,000+ LPs that has difficulty filling almost any deal. LPs have become accustomed to ignoring them because of the brand around their syndicate and dealflow. Alternatively, there are GPs who treat their syndicates like true venture funds with office hours, quarterly updates, transparency and a history of success in finding outliers. To succeed long-term, you really need great sector or stage deal flow, professionalism, communication and transparency - lean into all of it and treat all of your partners (founders, LPs, GPs) with the highest level of professionalism.

6. This is really freaking hard work

From the outside, I think a lot of people assume it is easy to put together SPVs. Just send out an email and funds come in. Let me tell you that SPVs is an extremely difficult business. If you’ve been an LP in a large number of syndicates over the last four years, hopefully this is clear as almost everyone leaves the ecosystem or moves to a fund model or reduces the number of SPVs they do. It’s freaking hard to do at scale.

As syndicate GPs, you spend a lot of time sourcing, trying to win allocation and putting materials together only to have zero assurance that your investors will even want to invest in the deal, and not because it’s not “a good deal” but rather because LPs have limited capital and their own criteria on what they’d prefer to invest in.

You may be thinking well this is sales, this is how the world works.

That’s partially true - if you’re a banker and taking on an engagement, there’s no guarantee you’ll get a success fee. If you’re selling a sales product, you have to talk to a lot of people to sell software. The big difference I’d argue is that there’s no salary coming in for syndicate GPs, meaning your only opportunity at any income or upside is closing. At least bankers get retainers and salaried sales execs receive salaries.

But of course there is a flip side, which is why we continue to do it… the paper markup of our carry today is in the many seven to eight figures.

If you enjoyed this piece, feel free to check out several other Last Money In articles that we referenced:

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!