- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- Wix vs Lovable: A Relative Valuation Case Study in Public vs Private Markets

Wix vs Lovable: A Relative Valuation Case Study in Public vs Private Markets

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

November 29, 2025

Wix vs Lovable: A Relative Valuation Case Study in Public vs Private Markets

Disclaimer: The author owns no Wix stock and has no known exposure to Lovable. This is not investment advice. This analysis is provided for informational and educational purposes only and does not constitute investment advice, financial advice, trading advice, or any other type of advice.

The AI-powered coding space is experiencing one of the most striking valuation disconnects between public and private markets in recent memory. Lovable—a two-year-old startup with approximately $200 million in ARR—just raised at a $6 billion valuation, making it worth more than Wix, a profitable public company with nearly $2 billion in ARR and a $5.3 billion market cap and parent co of Lovable competitor Base44.

How is a company with 10x less revenue valued higher than its established competitor? The answer reveals everything about how private and public markets have diverged—and who's actually getting the better deal.

First, the players.

Wix (NASDAQ: WIX) is a publicly-traded website building platform that enables users to create websites without coding. Founded in 2006, the company serves millions of customers globally and generates nearly $2 billion in trailing twelve-month revenue. In 2025, Wix acquired Base44, a fast-growing AI-powered no-code app builder that has scaled from near-zero to a projected $50M ARR by year-end.

Lovable is a private AI-powered application development platform that allows users to build software through natural language prompts—part of the emerging "vibe coding" or AI-native development category. The company reportedly raised funding at a $6 billion valuation in late 2025, achieving $200M ARR with 8 million users.

Both companies operate in the no-code/AI-powered development space, enabling non-technical users to build digital products. Yet their valuations tell radically different stories.

Last Money In Deals: We have made over 800 startup investments. Accredited investors & qualified purchasers within the LMI community can now gain access to our alternative investments such as venture, late-stage growth, and private equity through our deal flow sheet. Interested (it's completely free): Fill out this form.

🐦 Follow Us: Visit Alex’s Linkedin and Zach’s X account for constant updates Exclusive data from Sydecar, one of the industry's leading fund administrators, quantifies this transformation.

The Valuation Disconnect: 30x vs 3x

Lovable commands a 30x ARR multiple at its $6 billion valuation, while Wix trades at just <3.0x ARR with a $5.3 billion market cap. This represents a staggering 10x+ ARR multiple premium for the private company over the public comparable.

The math exposes the paradox: Lovable, with $200 million in ARR and 8 million users, is now valued higher than Wix, a profitable company generating almost $2 billion in trailing twelve-month ARR (~10x revenue scale).

The surface-level justification comes down to growth velocity and total addressable market (TAM). In this case, hypergrowth trumps scale, profitability, and market position.

Lovable achieved $100 million ARR in eight months—one of the fastest software startup growth rates in history—and doubled to $200 million ARR shortly after. This explosive trajectory allows venture investors to justify exceptional multiples by projecting exponential revenue expansion into a massive TAM. Wix, growing at a respectable 12-14% year-over-year, simply cannot match this velocity despite its superior profitability and established market position.

Here's where the narrative gets interesting: if Wix hadn't acquired Base44 this year, the valuation gap might be defensible. A mature company with low-double-digit growth arguably deserves a significantly lower multiple than an early-stage rocket ship with outlier growth.

But Base44 fundamentally changes this equation.

Wix—with its nearly $2 billion in trailing revenue and distribution base of millions of customers —now owns a fast-growing asset that directly competes with Lovable. Base44 has achieved hyperscale growth comparable to Lovable: from near-zero at the start of 2025 to a projected $50 million ARR by year-end. If Base44 were valued as a standalone business at Lovable's 30x ARR multiple, it would command a $1.5 billion enterprise value on its own.

The critical insight: Wix's market cap of $5.3 billion effectively bundles a $2 billion mature business with a $1.5+ billion hypergrowth asset—yet the market is valuing the entire entity at less than 3x ARR.

The Growth Trajectory Divergence

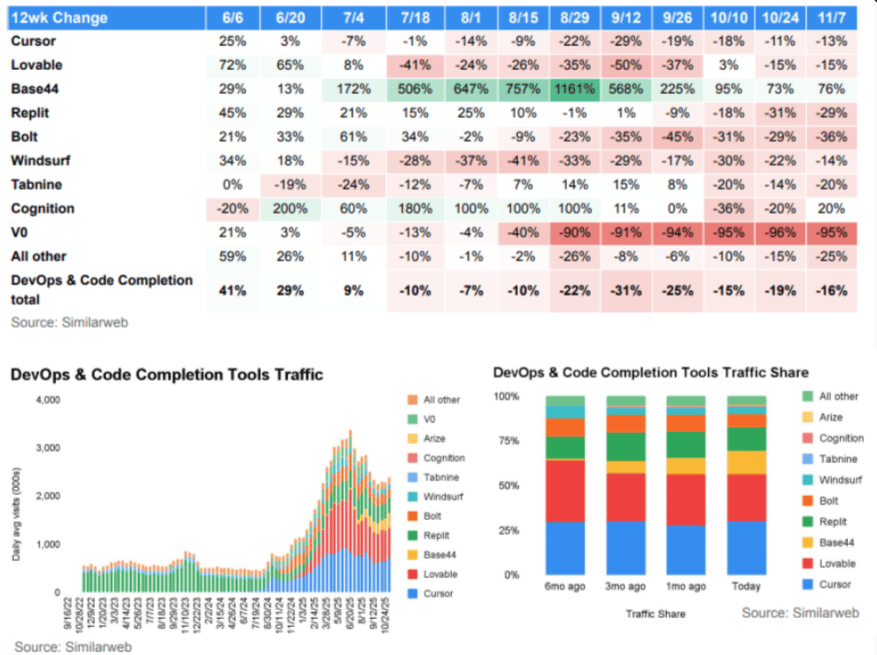

Additionally, recent data from Similarweb reveals another interesting dynamic: Base44 shows sustained hypergrowth with 76% traffic growth over the past 12 weeks, while Lovable's growth has decelerated with a 15% decline over the same period. This suggests that Base44's momentum is accelerating precisely as Lovable's growth is tapering off —a pattern that should narrow valuation multiples, but also not incredibly surprising given the scale of Lovable versus Base44.

Illiquidity Creates Pricing Power

Here's the reality behind private market valuations: while growth is the stated justification for multiple premiums, illiquidity actually creates the pricing power that enables founders to command extraordinary valuations.

When a company like Lovable raises capital, it might only offer $200-300 million in equity supply to investors, despite facing billions in demand from venture capitalists desperate for exposure to the next AI winner. This supply-demand imbalance gives founders extraordinary leverage to command valuations that would have difficulty surviving public market scrutiny.

The mechanics are simple but powerful: with limited allocation available and intense competition among investors to secure access to "the next big thing," private companies can effectively run an auction where the highest bidder wins. Investors rationalize paying massively premium multiples not purely because the fundamentals justify it, but because scarcity in private markets creates its own premium.

Public markets operate under completely different rules. They're the ultimate arbiter of value—continuous, real-time price discovery with unlimited liquidity. Anyone can buy Wix stock at any time, in any amount. There's no scarcity premium, no "we only have $X million to allocate" dynamic driving prices higher. The market simply prices in real time what it believes to be worth.

Lovable's Series A investors at a $1.8 billion valuation in July 2025 now hold an approximately ~3x paper gain in just four months. Meanwhile, Wix's market cap has fallen over 30% in the past year despite solid fundamentals, including the acquisition of fast-growing Base44. This contrast demonstrates how sentiment, liquidity constraints, and continuous price discovery compress public market valuations relative to private markets.

Which Market Offers Better Value?

The case for Lovable's premium rests entirely on sustained hypergrowth. To justify its current valuation, Lovable must grow 10x from its current ARR to reach Wix's revenue scale—and maintain premium multiples while doing so.

If Base44 weren't part of Wix's portfolio, this might be defensible. But Wix now owns an exceptionally fast-growing asset that directly competes with Lovable, alongside its mature, profitable core business. The market is effectively giving investors the Lovable comp (Base44) plus a $2 billion revenue business for a lower absolute valuation than Lovable commands alone.

For investors prioritizing asymmetric upside, private markets enable concentrated bets on potential category winners. Lovable's velocity—$100 million ARR in eight months—suggests the potential for multi-billion dollar revenue scale within years.

But the risks are substantial:

Multiple compression is inevitable: Even if Lovable hits $2 billion in ARR, its multiple will likely compress significantly as growth rates normalize. A company growing 200%+ can justify a 30x multiple; a company growing 10-40% year over year cannot.

Competitive threats are intensifying: AI model providers (Anthropic, OpenAI, Google) and new startups (Replit, Bolt, Base44) have launched competing tools and are heavily investing in the space. Category compression could erode Lovable's moat rapidly. The Similarweb data showing Lovable's recent growth deceleration suggests this may already be underway.

Public markets will be unforgiving: If growth tapers materially, public markets will reprice Lovable closer to the multiples that Wix and Squarespace currently receive—potentially destroying 80-90% of paper value for late-stage investors.

Why does this matter? If Lovable's growth stalls too quickly before reaching a much higher scale —or worse, turns negative—its equity value will evaporate.

Conclusion: Two Incompatible Frameworks—and What It Means for You

Public and private markets are valuing the same sector—no-code AI-powered application development—using fundamentally incompatible methodologies.

Wix represents the "show me" approach: prove sustainable unit economics, demonstrate margin expansion, and scale profitably. Even Base44's exceptional growth is heavily discounted until it reaches a much higher scale and proves durability.

Lovable embodies the "believe me" framework: bet on category transformation, accept extreme multiples as the cost of exposure to a potential outlier outcome, and hope to exit before growth normalizes and multiples compress.

Neither approach is inherently "wrong"—and to be clear, both companies (or neither) could massively outperform from current valuations. This analysis is not an argument for or against either company specifically. Rather, it's meant to underscore the dynamics at play between public and private markets, and to help investors understand part of what drives these extreme multiple discrepancies.

But if I had to choose one of these two options, I'm taking Wix. You get a profitable, cash-flowing business with 10x the revenue scale, plus direct exposure to Lovable's fastest-growing competitor in Base44. Much of the downside risk is mitigated by the mature core business, while the upside remains intact if Base44 reaches meaningful scale. At sub-3x ARR, you're not paying for that optionality—with Lovable, you're paying a premium that requires nearly everything to go right.

If you enjoyed this article, feel free to view our prior posts on adjacent topics