- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- Why 73% of Secondary Deals on Sydecar Now Flow Through Multi-Tier SPVs

Why 73% of Secondary Deals on Sydecar Now Flow Through Multi-Tier SPVs

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

June 21, 2025

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

We are extremely saddened by the news of Ali Jamal's passing this week. Ali started First Check Ventures, a syndicate and venture fund to back founders at the earliest stages. He was universally respected throughout the venture capital community by all who had the privilege of knowing him. Today we mourn the loss of an exceptional VC and friend of ours.

Rest in peace, Ali, you will be missed by all. 🙏

Why 73% of Secondary Deals on Sydecar Now Flow Through Multi-Tier SPVs

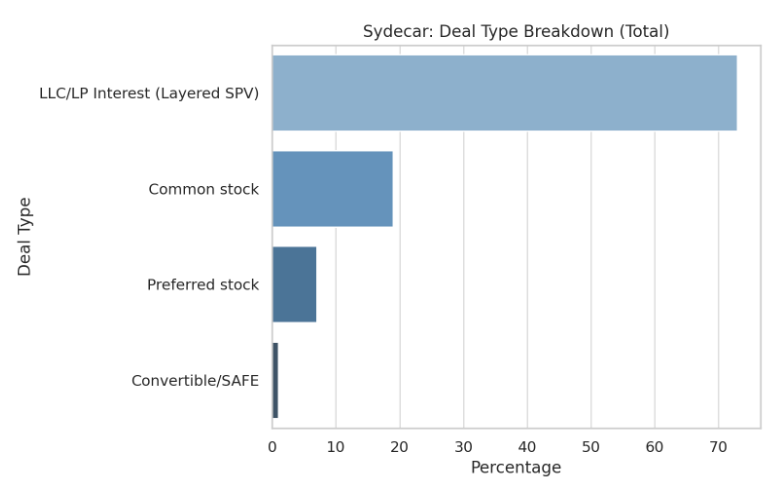

The secondary market has undergone a structural transformation, with layered Special Purpose Vehicles (SPVs) now dominating deal flow in ways that would have seemed unimaginable just a few years ago. Analysis of 345 secondary SPV deals completed between May 2024 and May 2025 reveals that 73% of secondary transactions on Sydecar now occur through multi-layer structures, fundamentally reshaping how investors access private market opportunities.

This shift represents more than just a structural preference—it's a strategic response to both an increasingly restrictive primary market environment and a fundamental liquidity crisis. As traditional exit paths have essentially evaporated—with IPO activity at historic lows and M&A volume drastically reduced—exit liquidity has increasingly shifted to secondaries.

Compounding this dynamic is the fact that companies are staying private far longer than historical norms. Previously, companies hitting $1 billion valuations would typically have gone public. Today, we see companies like SpaceX, OpenAI, Databricks, Anthropic, and Stripe reaching valuations exceeding $50 billion while remaining private. This creates enormous pent-up liquidity demand for names that simply wouldn't have existed in previous market cycles, as these companies would have been publicly traded and freely accessible. We're witnessing this trend not just in the explosion of dedicated secondary funds, but as mentioned, in the proliferation of syndicated secondary opportunities that didn't exist at scale just years ago.

Simultaneously, as issuers tighten controls around secondary trading and impose stricter penalties on investors who sell positions freely, sophisticated market participants have found layered SPVs to be the most effective option for accessing this critical liquidity source.

💸Last Money In Deals: We have made over 800 startup investments. Accredited investors & qualified purchasers within the LMI community can now gain access to our alternative investments such as venture, late-stage growth, and private equity through our deal flow sheet. Interested (it's completely free): Fill out this form.

👜Try Deal Sheet for Free: Want to join hundreds of subscribers in trying Deal Sheet, our premium newsletter that provides you access to the top venture deals with discounted carry. Try Deal Sheet for free for 7 days here.

🐦 Follow Us: Visit Alex’s Linkedin and Zach’s X account for constant updates Exclusive data from Sydecar, one of the industry's leading fund administrators, quantifies this transformation.

The Numbers Tell the Story

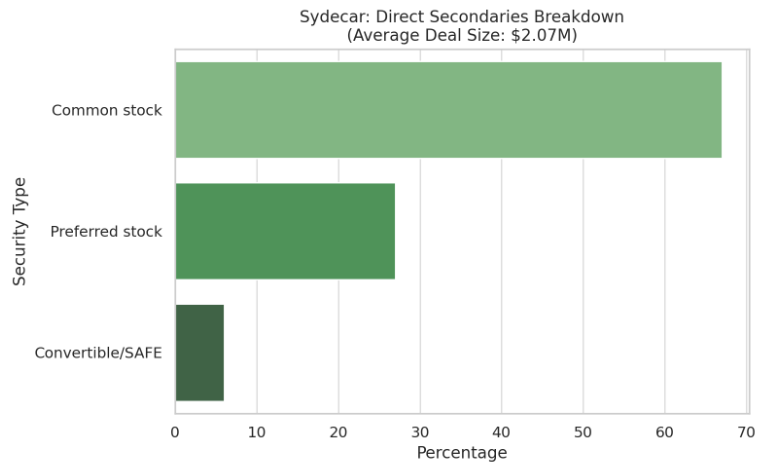

Security composition differences are particularly telling: direct deals favor common stock (67%) versus preferred stock (27%), which makes sense given that the number of common sellers (founders, employees) typically is much larger that the number of preferred sellers (investors).

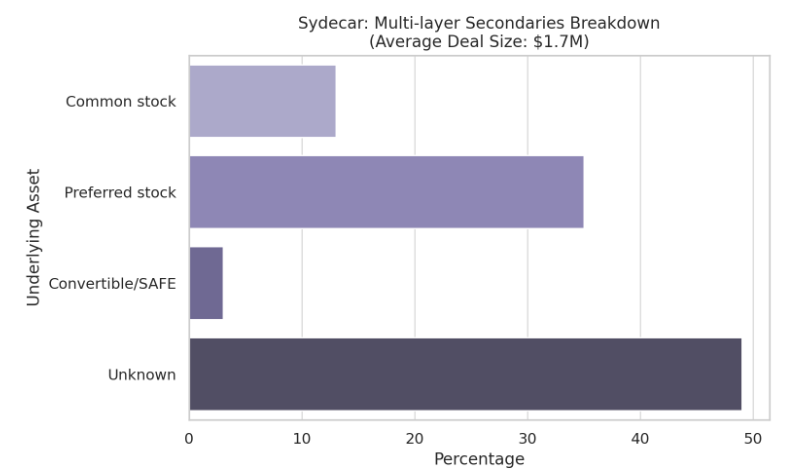

Within the available data, layered structures show a preference for preferred stock. These structures provide investors with strategic advantages, including enhanced privacy and helping preserve valuable relationships with management teams.

The LP Evolution: New Access, New Considerations

For limited partners, layered SPVs present both unprecedented opportunity and new considerations. The upside is access to best-in-class names that would otherwise remain completely inaccessible, particularly in a market where direct allocation opportunities have become increasingly scarce. These structures democratize access to elite investment opportunities.

And notably, this democratization has unlocked massive value creation for a new class of investors. Many LPs are reporting paper gains that dwarf their public market returns, accessing growth stories that are more difficult to find in the public markets. The layered SPV structure, while complex, has become a potential equalizer given the lack of friction to owning a piece of a high flying startup.

However, like any new innovation, there are risks. Stacked fees across multiple layers can erode returns, while the lack of transparency around underlying assets could create due diligence challenges. LPs often find themselves several degrees removed from the actual investment.

Key Protective Measures for Limited Partners: LPs should prioritize due diligence on the sponsor's track record. Ensure you understand the multi-layer fee breakdowns and ensure you understand the total cost structure, including management fees, carried interest, and any performance-based compensation at each level.

Freer Trading Won't Solve Everything

While issuer control drives much of the layered SPV phenomenon, the structural forces at play run deeper than company restrictions alone. Even if private companies allowed shares to trade as freely as public company stock, the layered syndication model would likely persist due to the economics that benefit major VCs.

The reality is that large VCs have discovered a lucrative new revenue stream in syndication fees. These firms collect upfront premium fees, management fees, and carry economics when they syndicate out allocations through SPV structures. This creates powerful financial incentives to maintain the current system regardless of issuer policies. Major VCs are essentially getting paid twice: once through their traditional fund economics, and again through the fees generated by breaking down and redistributing additional allocations that go beyond their fund investment.

This dual revenue model means that even in a hypothetical world where companies imposed no secondary trading restrictions, sophisticated investors would likely continue using layered structures simply because they're profitable.

Why Layered SPVs Are Here to Stay

Today, the layered revolution thrives because multiple parties have incentives to make it necessary. Companies have chosen tighter control over their cap tables, optimizing for future fundraising rounds rather than shareholder liquidity. Meanwhile, large VCs have discovered that syndication generates substantial fee income beyond their traditional economics.

The irony is clear: the more restrictive startups become about direct secondary trading, the more opaque and layered the actual trading becomes. And now, with the large VCs benefiting from this complexity, the incentives to maintain these structures extend sometimes beyond issuer control.

For LPs, this dynamic creates a fundamental trade-off that defines the modern private market landscape. Access has never been better—sophisticated investors can now participate in opportunities that were previously impossible to reach. But that access comes at the cost of transparency. The market has essentially chosen breadth of access over clarity of structure, creating a system where more investors can participate, but with less direct control and understanding of what they actually own. This isn't necessarily good or bad—it's simply the new reality of how elite private market opportunities get distributed in the new era.

If you enjoyed this article, feel free to view our prior posts on adjacent topics

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!