- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- The Misaligned Syndicate Incentive Structure

The Misaligned Syndicate Incentive Structure

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

April 24, 2024

Last Money in is Powered by Sydecar

Sydecar is a frictionless deal execution platform for emerging venture investors. We make it easy for anyone to launch SPVs and funds in minutes, with automated banking, compliance, contracts, tax, and reporting so that customers can focus on making deals and building relationships. Fill out our unique form to get to the top of the line here.

Deal Sheet = The.Best(& investable).Deals.Period.

Curated & Discounted SPVs directly to your inbox

Deal Sheet is a paid weekly newsletter that delivers the best startup investment opportunities weekly. These deals are being syndicated by 20+ of the best and most active syndicate leads we’ve worked with. All Deal Sheet deals include discounted carry (10% carry versus standard 20%).

Deal Sheet pricing will be going up on May 1st! Lock in your rate today!

Check out our new Deal Sheet overview deck here!

The Misaligned Syndicate Incentive Structure

Guest post by Phil Nadel of Forefront Venture Partners

This week, Last Money In is excited to share a guest post from one of our colleagues Phil Nadel, who leads Forefront Venture Partners. In 2024, Last Money In decided it would be to the great benefit of readers to have five to ten thought leaders from around the Syndicate/Emerging Fund GP ecosystem write a post sharing a unique perspective on an SPV related topic (and with no editorial overview from our end - we want all participating guest authors to write on a topic that speaks to them).

More on Forefront: Forefront Venture Partners formed one of the first syndicates on AngelList about 12 years ago. They have invested in more than 200 rounds in over 100 companies since then. Additionally, they started a rolling fund about 3 years ago. Given his extensive experience across models (SPVs/Funds) and having seen the evolution of the ecosystem over the last decade, Phil has kindly offered to share his unique perspective with Last Money In readers today.

In this post, Phil is covering his POV on the incentive structure in the SPV ecosystem - where it may be misaligned (and why) and alternatives that exist for LPs. Of note, all of the commentary below represents Phil’s perspective and are not reflective of our own view, as is the case for many hot topics.

Now onto Phil’s post…

The Misaligned Syndicate Incentive Structure

The initial idea behind syndicates was to enable angel investors to tap into the deal flow, rigorous due diligence, and negotiating leverage of an experienced general partner (GP) and invest alongside the GP on the same terms in exchange for a carried interest.

Proliferation of "High Volume, Low Quality" Syndicates

There has been a rapid increase in the number of syndicates available on AngelList, and I characterize many of these as "high volume, low quality." They conduct very little substantive due diligence on the companies they syndicate and may never have even spoken with anyone at the company. They are given allocations in deals by VCs or other investors, often without the knowledge or approval of the startup they are investing in.

Worryingly, the GPs of these funds have adopted a strategy of syndicating as many deals as possible, investing very little of their own money in each, and relying on the law of averages in hopes that some investments will work out so the GP can earn a carried interest (“carry”). This has resulted in some syndicates recklessly offering up 5, 10, or even more deals per week. Substantive due diligence at this velocity is, as a practical matter, impossible. In contrast, we typically invest in only 10 deals per year after rigorously vetting each opportunity. We firmly believe that more scrutiny upfront helps significantly reduce the number of strikeouts (more info here).

Divergence of Interests Between LPs and GPs in Syndicates

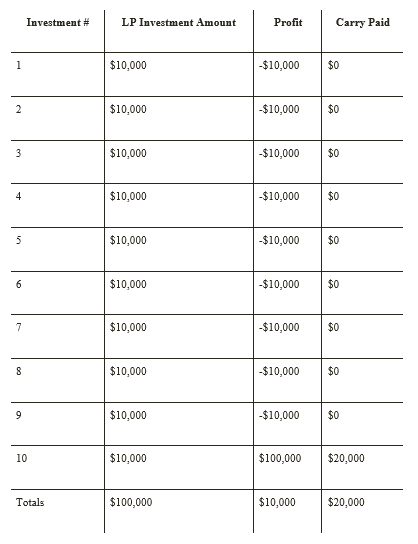

I started to sound the alarm bells on this issue more than two years ago (read my article here), but since it has become insidious (and increasingly prevalent, to an almost unbelievable degree), I am writing to warn you again. High-volume, low-quality, factory-style syndicates can lead to a dangerous divergence of interests between limited partners (LPs) and GPs. The syndicate GP earns a carried interest on all investments that result in a profitable exit, regardless of the total portfolio performance. Here is an example that starkly illustrates how this structure can result in poor results for LPs but lucrative outcomes for GPs (let’s assume 20% carry for all examples):

In this example, the LP invests a total of $100,000. They lose $10,000 on 9 deals and earn a profit of $100,000 on just one deal. The result is an overall portfolio profit of $10,000, right? Wrong - after factoring in the $20,000 carry paid on the one profitable deal, the LP is actually left with an overall portfolio loss of $10,000.

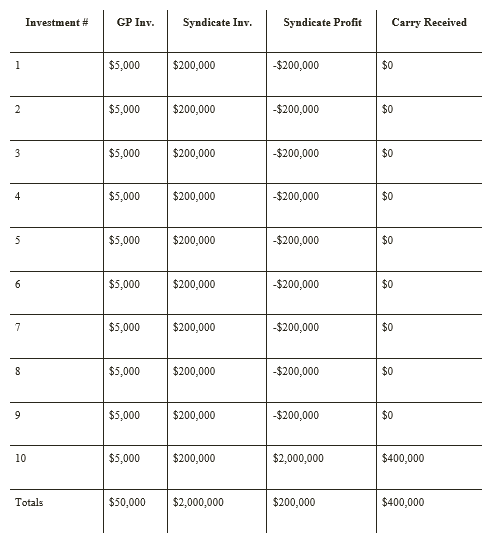

In the following chart, you can see how the math works out for the GP in this scenario.

The GP syndicates 10 deals and raises $200,000 for each but invests only $5,000 of their own money into each one. Assume the same facts: 9 out of 10 investments result in a complete loss while one investment results in a 10x profit. The LPs each lose money overall after paying the carry, but the GP earns a $400,000 carry. Can you see how incentives and interests are misaligned? The GP has an incentive to syndicate as many deals as possible in the hope that some will work out well and they will earn a large carry. As long as they can continue to entice new and existing LPs to invest, they have an opportunity to profit handsomely without regard to whether the LPs lose money. In this model, a GP’s profit driver is volume, not quality, while an LP depends on quality outcomes to drive favorable financial results. With such flawed incentives, it's no surprise that substantive due diligence often falls by the wayside as GPs are motivated to prioritize raising more funds for more deals.

Things get even worse for the LPs when you consider that since the GPs typically have no substantive relationship with the startups, they almost never receive investor updates from them. That means the LPs in these syndicates have zero visibility into the true performance (or lack thereof) of the companies they invest in. And they have no knowledge of how they can assist the startups they invest in, since these requests for help are almost always included in investor updates.

This is bad for LPs and bad for startups.

Rolling Funds: Aligned Interests Between LPs and GPs

Now let's contrast this with a rolling fund. Like with a traditional venture capital fund, rolling funds earn carry only if there is an overall, portfolio-wide profit. Critically, carry is computed not on a deal-by-deal basis as it is with syndicates, but on the entire portfolio performance as a whole. The GP earns no carried interest unless the LPs earn a net profit on all investments in the fund's portfolio. Therefore, the GP has a strong incentive to be highly selective in choosing which startups to invest in and to conduct extensive due diligence. The GP's interests are squarely aligned with LPs' interests, as it profits if and only if the LPs earn a net profit.

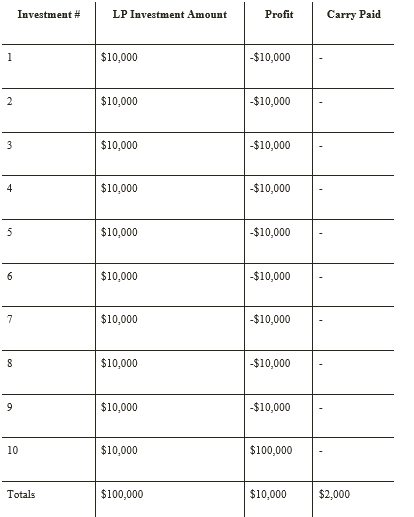

Here’s the same chart as above, but assuming the LPs are in a rolling fund.

As you can see, assuming the exact same investment results, the LP earns a profit of $8,000 after paying the carry. The difference is that the carry is only $2,000 instead of $20,000 because it is computed on the profit earned from ALL investments made by the fund.

I would like to highlight one more important difference between syndicates and rolling funds. In our 12 years experience managing a large syndicate, we have found that many deals are unavailable to a syndicate that are available to a rolling fund. This is due to a few factors:

Some deals need to close quickly and there is insufficient time to run a syndicate.

Some companies require the certainty of a specific investment amount upfront that syndicates are unable to provide because of their variable nature.

Often, founders are unwilling to share sensitive information about their companies with a broad audience (e.g. all LPs in a syndicate).

The result is that syndicate LPs are frequently unable to participate in the most selective and promising deals.

There are other ways in which a GP’s interests are divergent from its LPs’ (see here), but the syndicate structure exacerbates the problem when dealing with GPs looking to take the easy way out.

The take-away here should not be that investing in any syndicate is a bad idea. When syndicates are managed diligently, run scrupulously, and oriented towards holistic returns and effective custodianship of LPs’ funds, they can work well. But, I advise extreme caution and serious inquiry into the syndicate GP’s track record, cadence of deals, and rigor of due diligence. In order to have a higher degree of certainty that your interests are aligned with the GP’s and that you gain access to the more highly coveted and selective deals — and that there exist no structural “exploits” that can be taken advantage of by the high-volume, low-quality approach — I encourage you to consider investing in a rolling fund led by a trusted and experienced GP.

Phil Nadel is the Co-Founder and Managing Director of Forefront Venture Partners and the Forefront Venture Fund (rolling fund). Follow him on Twitter: @NadelPhil or on Medium at https://medium.com/@pnadel or connect with him on LinkedIn.

If you enjoyed this article, feel free to view our prior posts from guest GP authors

Last Money In is Powered by Sydecar

Sydecar is a frictionless deal execution platform for emerging venture investors. We make it easy for anyone to launch SPVs and funds in minutes, with automated banking, compliance, contracts, tax, and reporting so that customers can focus on making deals and building relationships.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!

✍️ Written by Zachary and Alex