- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- Even Founders Fund Can't Speed Up VC Liquidity

Even Founders Fund Can't Speed Up VC Liquidity

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

February 28, 2026

Even Founders Fund Can't Speed Up VC Liquidity

I've been running SPVs since 2020. In those six-plus years, the single most consistent frustration I hear from LPs is about liquidity — or more accurately, the complete absence of it. And I get it. I’m frustrated. You write a check, you're excited about the company, maybe it raises a few more rounds, the markup looks great on paper… and then nothing. No cash back. For years. Or worse, maybe the Company stalls out and dies before realizing any distribution.

But unless you're playing exclusively in pre-IPO markets or you get absurdly lucky with an early, meaningful exit, this is just venture capital. Liquidity takes a long time.

Exhibit A: Founders Fund

Take a look at Founders Fund's reported returns. These are objectively amazing returns. Most top-tier funds can't consistently return 2-3x+; Founders Fund has reportedly delivered ~3x+ across its first five funds, and Funds 6, 7, and 8 look reasonably strong relative to their vintages.

But here's the thing — even at Founders Fund, no fund of theirs since roughly the 2014 vintage has returned meaningful DPI if any at all. For anyone unfamiliar, DPI measures how much actual cash a fund has sent back to its investors relative to what they put in. It's the number that matters a lot to LPs because you can't deposit a markup.

Their last five funds — spanning 2017, 2020, 2020 (growth), and 2023 vintages — have returned virtually nothing, and in some cases literally nothing, back to LPs. That's a near decade-long hold on the 2017 vintage with zero distributions. And again, this is one of the best-performing firms in the industry.

This Is Normal

This is par for the course. Without naming names, one of the most prominent seed investors in the ecosystem — a fund everyone in this world would recognize as top-caliber, with multiple vintages of elite performance to back it up — told me he was essentially living paycheck to paycheck for close to a decade before his early bets started going public and actually distributing.

VC is the opposite of fast riches. It carries a risk profile comparable to crypto but without the liquidity, and with a timeline that stretches a full decade longer before you see real cash. It's brutal. And it's one of the reasons I feel both lucky and, in some ways, a bit cursed to have started investing early.

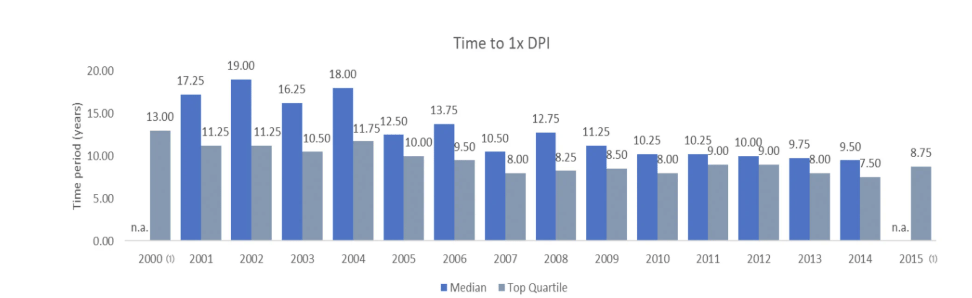

What the Data Says

Using Cambridge Associates' quarterly DPI data from March 2000 through March 2024, we can look at how long it has historically taken VC funds to return 1.0x of invested capital across vintages from 2000 to 2015.

The data confirms what the anecdotes suggest: most VC funds take close to a decade, and often longer, to return investors' capital.

In the first two to three years, DPI is effectively zero — the fund is still writing checks. By years three to five, a typical fund might show around 0.2–0.3x DPI, which is completely normal and not a red flag. Upper-quartile funds generally need about eight years to hit 1.0x DPI, while median funds take roughly 9.5 years or more. Some vintages stretched to 13–19 years. Even top-performing funds that ultimately reach 2.0x+ DPI usually don't get there until years seven to ten, and sometimes much later given extended fund lives and longer exit timelines.

Fast distributions are the exception in <7 year timeframes, not the rule.

So What Should You Do With This?

If you're an LP in SPVs or VC funds, a few things worth internalizing:

Plan accordingly. Don't deploy capital you can't afford to lock up for a decade. The odds of getting anything meaningful back in the first several years are low, and that's true even for great managers.

Match the strategy to your risk appetite. If shorter liquidity timelines matter to you, pre-IPO and later-stage opportunities might be a better fit. If you're comfortable with a long horizon and want to chase the biggest potential multiples, seed-stage investing might suit you — just go in with eyes wide open about the wait period, which again is probably 10 or more years to receive anything meaningful.

Don't be surprised by the silence. I've watched LPs churn out of venture every few years because they got excited, wrote checks, and then didn't fully appreciate just how sparse distributions would be. Retail investors have really only had meaningful access to venture for about a decade. The patience required is still a lesson the market is learning.

The Liquidity Problem Isn't Solved Yet

The good news is the secondary market is maturing. Brokers have gotten meaningfully better at creating liquidity for top-tier names, and dedicated secondary funds are becoming more abundant, which is a real step forward. But there are significant limitations. That liquidity is heavily concentrated in the top 30-40 most recognizable companies — and even that activity tends to dry up or go quiet in bear markets.

For everyone else, the options are thin. Fund managers face an incredibly difficult time selling positions even with discretion, and for retail LPs, there's effectively no practical pre-M&A/IPO exit path. As a retail LP, even if you wanted to stomach a discount and find a buyer, the current infrastructure makes the process expensive, time-consuming, and operationally painful for GPs — so don't assume your manager can just flip a switch and get you out. I can’t.

Speaking from experience, even when I've tried to facilitate secondary sales, half the LPs push back, which means the incentive for managers to run these processes isn't always there unless the outcome is clear-cut — and in a highly illiquid private market, which is rare. Whoever ultimately cracks VC liquidity beyond the top names will be solving one of the biggest structural pain points in the asset class. Until then, the lack of liquidity is sometimes a feature and sometimes a curse — either way, plan accordingly.