- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- We’re Closing $30M+/year in SPVs as a Solo GP, Why Would I Ever Start a Fund?

We’re Closing $30M+/year in SPVs as a Solo GP, Why Would I Ever Start a Fund?

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

June 26, 2024

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

Fill out our unique form to get to the top of the line here.

Deal Sheet = The Top VC Deals to Your Inbox Every Single Monday

On Monday we shared our 20th Issue of Deal Sheet that contained 5 investable deals from pre-seed to series D and co-investing alongside Tiger Global, D1, Thrive Capital, 8VC, Redpoint and many more! To get access to these deals at 10% carry you can sign up for Deal Sheet here or book a call to learn more!

We’re Closing $30M+/year in SPVs as a Solo GP, Why Would I Ever Start a Fund?

I started in the syndicate ecosystem as a GP in 2020. Notably I was an LP in multiple syndicates for several years prior, participating in my first angel syndicate in 2018. At the time I had just finished a stint working for three years at an investment bank in San Francisco and was starting an MBA. I was five years out of undergrad and at the time was considering either attempting to get into private equity (PE) or break into venture capital (VC). I had interest in both, but wasn’t sure.

I dropped out of my MBA program fairly quickly (3 months in) as it turned out I wanted to work, and that Summer (2018), I was given two separate summer offers, one was to work for an awesome VC syndicate in LA (still to this day, I believe they are the #1 syndicate) and a middle market (MM) private equity fund in New York. Notably, the VC syndicate in LA was completely unpaid, while the MM PE fund was going to pay me a good amount of money at the time. I went for the VC fund and so my syndicate learning from the GP side began, but at the time I candidly didn’t think I’d end up running one.

After this internship, I went on to join a growth fund in LA in 2019, and then ended up leaving in 2020 to start Calm Ventures. This year, in an extremely difficult SPV/VC market, we're pacing to deploy ~$50M in capital in 2024 via 120+ SPVs. This begs the question and one I’m asked extremely often - why not start a fund?

This is the reality.

When I first started syndicating, I had very little relative experience to start a fund - less than one paid year of VC experience, and I didn’t have the operating background to position myself as an expert in anything. The idea of going out to raise a fund at the time wasn’t even a part of any internal conversation - the only paths forward I was considering were 1) join a different fund or 2) start a syndicate.

I had already experienced what it was like working for a traditional VC fund, and while I learned a lot, I had the entrepreneurial bug to start my own VC, which led me to syndicates. Similarly I had also interned for a syndicate and been an LP in syndicates for several years - so I understood the landscape and could solve the problem of how to find LP capital.

I ended up going the syndicate route - it broke down all of the barriers to get started building your own venture firm and this thesis (for me) was right.

The first deal we did happened fast and we raised over $350,000 for it. I was getting almost ~20% of the carry economics; if we were able to 5x the capital on this single deal (it was a hot Series A company), I could make $280,000 in carry on this deal alone, which was more than I was making all in annually at my prior fund, and again this was just on one deal - for context we are doing 120+ deals a year now.

This first year in 2020 we ended up deploying $12M (vintage est. at $29M value today); given funds are typically deployed over three years, it was basically as if I had a $36M solo VC fund (deploying $12m/year for 3 years = $36M Fund) in my first year syndicating. Or at least that was my thinking at the time.

And candidly, I think if I had even tried to raise a fund back then it would have taken over a year and only been a micro fund ($1-10m in capital over ~3 years); relative to syndicates, it didn’t make any sense from an economic standpoint.

After having some fairly early success building a track record (and a lot of luck and great partners) - again the conversation of starting a fund in 2021 wasn’t of interest.

To break down the pros/cons at the time:

In my first year (2020), we deployed $12M or essentially, I had a $36M solo fund

The carry economics on SPVs were superior to that of a fund - all economics are deal by deal and not on a fund level; in other words, your losers don’t go against your winners

I could have a flexible mandate and invest across stages and industries (most funds do not have this and have a stage and/or sector focus); I was interested in b2b software but also interested in consumer and other sectors - the SPV structure gave me flexibility here to explore these industries

I was building a track record and network to launch a fund in a better position at a later date if I so choose

Some cons were:

I was giving up a salary and fees

I was constantly raising capital (it is still never ending and a lot harder today)

I was at the whims of the market; if macro turned out it’s likely the SPV market would dry up

I wasn’t able to construct a portfolio the way I wanted as I wasn’t controlling the capital (the LPs were) (more on this in “Why You Should Discount a Syndicate Lead’s Performance”)

But things continued to go relatively well from a process standpoint since that first year. In 2021, we deployed over $85M (or essentially a $250M+ solo fund) and this year, in a horribly difficult VC/SPV market, we may still end up deploying ~$50M (essentially a ~$150M solo fund).

However my thoughts today, on syndicate versus fund are much different than in 2020/2021 when I first started out and now having been through what feels like many cycles compressed into a 5 years from (2020-present), the answer is more nuanced.

So to answer the question, does it make sense to start a fund today?

A syndicate is a way to build quickly; a fund, albeit much slower to get started, is a way to build something much bigger - and not just from an AUM standpoint. At $30m-50m likely deployed this year, I would not raise a fund to go big at first / I would only raise a fund to build a world class firm.

I’ll be the first to admit that having a fund requires a different level of discipline due to a mix of more aligned carry incentives and constraints. When your losers go against your winners on the carry component, you need to think much more deeply about your model (e.g. portfolio construction); similarly when you have limited shots on goal and limited capital, every investment requires stronger conviction.

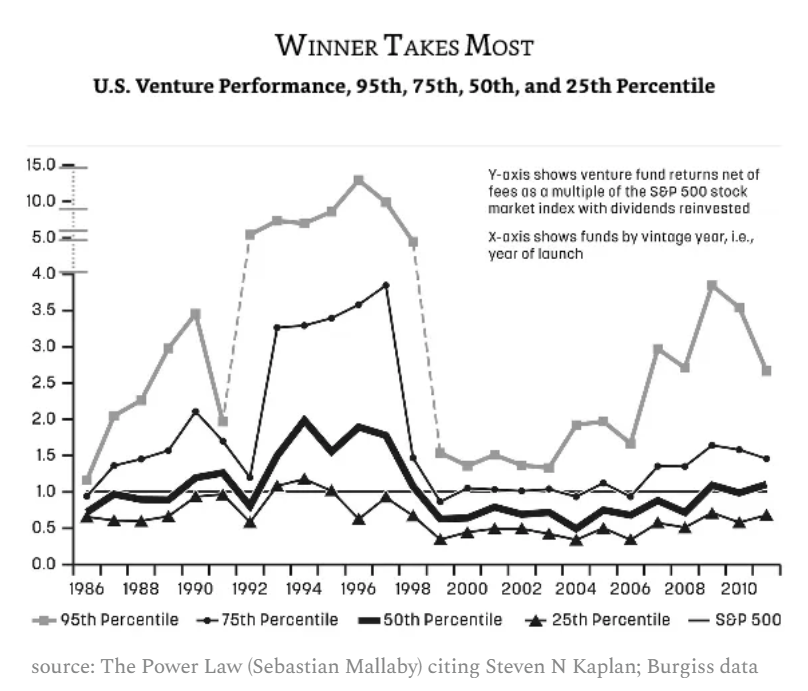

And venture capital as a fund is a much different business when your losers go against winners. Yes, venture capital generally outperforms every other asset class but the dispersion of returns is wider in venture than anywhere else with almost half of funds returning 1x capital or less…meaning if you go the fund route, you better be best in class at your job to receive any meaningful upside.

And sometimes being great at your job is outside of your control - I know many people that launched funds in 2021 that will not perform well because they deployed too much at the top of the market - that’s mostly on them for a lack of discipline/restraint and partially just tough luck. But most of those GPs won’t see a dime of carry with many not able to raise fund II.

If I were to raise a fund today, the opportunity cost is also substantial - given the effort, I would pull back syndicating almost completely, which means I’m basically giving up a $100M recurring fund ($30-40m/year = $100m (ish) fund likely) and giving up superior carry economics in the process.

However what I’d gain by starting a fund could be extremely meaningful.

First and above all - I would have full discretion over capital deployment - something syndicate GPs do not have. I’d go slower, but build something potentially much bigger. With management fees, I’d be able to hire top talent and actually pay myself a salary. With constraints, it’s likely LPs will do better; with structure we could provide much more support to all stakeholders (founders, LPs, partners), something that is extremely difficult today in a syndicate model with minimal recurring income. With full control over capital allocation, I could build a portfolio that optimizes strategy and outcomes. Candidly I’ve thought so deeply about so many issues across venture the last five years that if we went the fund route, the only goal would be to attempt to become world class in terms of returns - something I’d argue you can not do with a syndicate (again reference Why You Should Discount a Syndicate Lead’s Performance). Otherwise it is not worth it.

So to summarize the pro / con argument further.

Venture Fund Pros:

Full control over investment decisions and fund management

Potential for higher returns and larger management fees

Ability to build a strong brand and reputation in the industry

Opportunity to provide more comprehensive support to portfolio companies

Build a world class firm, albeit slower

Venture Fund Cons:

Requires significant capital to establish and operate the fund

Higher regulatory and compliance requirements

Greater responsibility and accountability to limited partners (investors)

Much longer fundraising process and more complex fund structure

Arguably worse economics against a syndicate from the carry component (although with full discretion over capital deployment, I think the economics would end up better)

Fund size would be significantly less than dollars I’m able to deploy today (most likely)

VC Syndicate Pros:

Lower barrier to entry, as it requires less capital (for me no capital) to start

More flexibility in terms of investment amount, criteria and participation

Less regulatory and compliance burden compared to a venture fund

Much easier to leverage the deal flow and due diligence of other GPs (syndicates are highly collaborative)

Deal by deal economics on the carry component

VC Syndicate Cons:

Limited control over how much we can invest, as the LPs typically drive the amount raised and thus some adverse selection in the process

Potential for lower returns as GPs have less control over investment decisions (again LPs drive $ commitments)

No management fees (typically)

Less ability to provide hands-on support to portfolio companies and LPs - with minimal recurring cash due to a lack of management fees, providing large levels of support are near impossible

A highly cyclical market - even more so than venture capital traditional fundraising I’d argue

To wrap, for some, the Fund route is the way to go, but for me today, I love syndicates and am doubling down on the ecosystem both on the syndicate side and on the content side with Last Money In and Deal Sheet. I get why this route doesn’t make sense for some, but for us, it’s right where we want to be.

If you enjoyed this article, feel free to review our prior articles that share our more personal anecdotes:

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!