- Last Money In - Newsletter on Venture Capital Syndicates

- Posts

- Sydecar Data Reveals: The Explosive Growth and Concentration of Secondary SPV Markets

Sydecar Data Reveals: The Explosive Growth and Concentration of Secondary SPV Markets

a newsletter about VC syndicates

Alex Pattis & Zachary Ginsburg

March 08, 2025

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

Deal Sheet Free Trial. Start your 7 day trial here!

Deal Sheet provides accredited investors:

Access to some of the best startup opportunities across the VC syndicate ecosystem (est. 150-200 deals on Deal Sheet per year) and

All Deal Sheet deals come at discounted carry – all opportunities on Deal Sheet are listed at 10% carry (versus 20% standard) with select opportunities (at our discretion) at 0% carry.

Try the free trial today here!

Sydecar Data Reveals: The Explosive Growth and Concentration of Secondary SPV Markets

The Evolution of Private Markets

The past decade has witnessed a fundamental shift in how high-growth technology companies approach public markets. With the median time to IPO extending from 4-5 years in 2000 to over 10 years today, the most coveted startups now remain private significantly longer, building multi-billion dollar valuations before considering public offerings. This structural change has catalyzed explosive growth in secondary markets, where investors can access shares of private companies without waiting for an IPO.

The secondary market ecosystem is relatively young—just two decades ago, Barry Silbert founded SecondMarket while working at Houlihan Lokey, having identified a critical gap in financial infrastructure: the absence of a centralized marketplace for trading illiquid assets. What began as a niche solution has transformed into a thriving marketplace. By the end of 2024, secondary transaction volume is estimated to have surged past $150 billion, shattering previous records and representing a 35% compound annual growth rate since 2019.

This dramatic expansion reflects both necessity and opportunity—necessity for early shareholders seeking liquidity, and opportunity for investors eager to participate in value creation that increasingly occurs before companies go public.

The Rise of Structured Secondary Transactions

The mechanics of secondary transactions have evolved significantly in recent years. While historically these trades occurred directly between individual shareholders and institutional buyers, the market has decisively shifted toward more sophisticated structures—particularly Special Purpose Vehicles (SPVs). These purpose-built investment entities allow multiple investors to pool capital for targeted secondary acquisitions, providing enhanced governance, administrative efficiency, and access to opportunities that might otherwise require prohibitively large minimum investments.

💸Last Money In Deals: We have made over 800 startup investments. Accredited investors & qualified purchasers within the LMI community can now gain access to our alternative investments such as venture, late-stage growth, and private equity through our deal flow sheet. Interested (it's completely free): Fill out this form.

👜Try Deal Sheet for Free: Want to join hundreds of subscribers in trying Deal Sheet, our premium newsletter that provides you access to the top venture deals with discounted carry. Try Deal Sheet for free for 7 days here.

🐦 Follow Us: Visit Alex’s Linkedin and Zach’s X account for constant updates Exclusive data from Sydecar, one of the industry's leading fund administrators, quantifies this transformation.

Exclusive data from Sydecar, one of the industry's leading fund administrators, quantifies this transformation.

Their platform recorded a remarkable 198% increase in total deal volume in 2024 compared to 2023, but the growth in secondary-focused SPVs was even more dramatic. Capital raised specifically for secondary transactions through Sydecar's SPV infrastructure surged by 470% during this same period—nearly five times the previous year's volume.

This acceleration appears to be gaining momentum rather than plateauing. Based on first-quarter activity metrics, Sydecar's projections indicate 2025 is on pace to double 2024's already record-setting secondary transaction volume. This trajectory suggests that structured secondary investments through SPVs are becoming institutionalized as a core strategy for accessing private market opportunities.

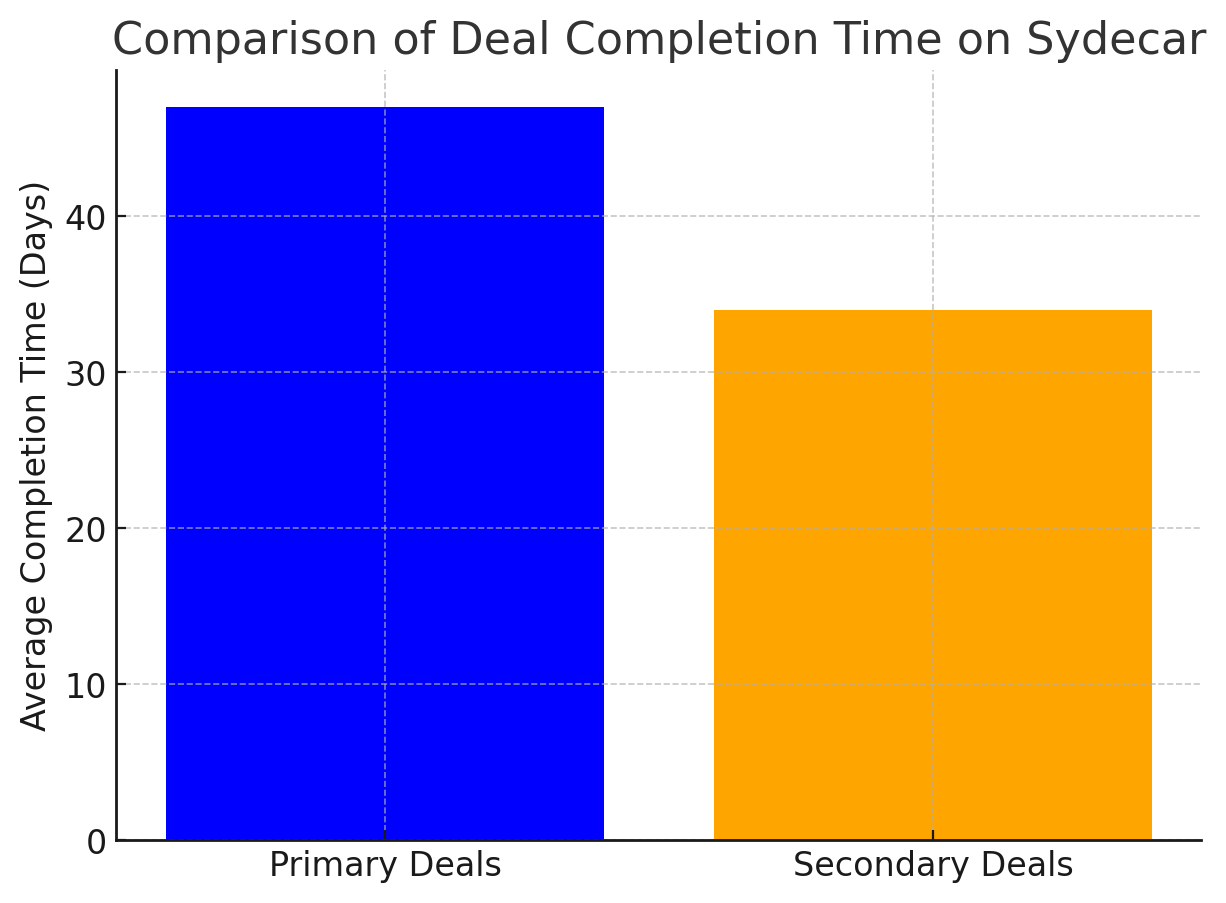

The Efficiency Advantage

A compelling and unexpected finding in Sydecar's data is the remarkable efficiency of secondary transactions.

Secondary deals are completed in just 34 days on average—28% faster than the 47-day timeline typical for primary transactions on the platform. This efficiency differential challenges conventional wisdom (including mine) that secondary transactions, with their potential transfer restrictions and approval requirements, would take longer to execute than primary investments.

This accelerated timeline signals a maturing ecosystem where market participants have developed standardized processes, documentation, and best practices. Secondary transactions once required custom legal work and complex negotiations for each deal, but the market has evolved toward repeatable structures and streamlined workflows. Sophisticated intermediaries, specialized legal counsel, and purpose-built infrastructure providers have emerged to reduce friction, enabling deals to close with unprecedented speed.

The Speed Paradox

Anecdotally, we sometimes see contradictory patterns on the ground—certain issuers have become increasingly restrictive around share transfers, and hot new primary financings can occasionally delay closings for secondary rounds targeting the same companies. These exceptions are worth noting, but they don't undermine the broader efficiency trend.

When you break down the transaction process, the speed advantage makes sense.

Primary financings involve multiple complex stages: launching the fundraise (and with it our SPV), raising capital, issuers negotiating terms with the lead, building out comprehensive legal documentation, securing board approvals, and finalizing closing conditions. In all, these primaries can stretch months as a result.

Secondary deals, by contrast, have a much more streamlined path to closing. When investor demand is strong and the issuer maintains reasonable transfer policies—these transactions can move from launch to wire quickly as supported by Sydecar’s data. The deal parameters are often clearer, the documentation more standardized, and the approval processes more established.

To underscore, this efficiency gap isn't universal, especially when primary raises muddle up secondary processes, but it's becoming the rule rather than the exception as the secondary ecosystem matures.

The Elite Eight: Unprecedented Investment Concentration

Perhaps the most remarkable trend—though less surprising to those of us who track the market closely—is the extreme concentration of investment activity among an elite cohort of companies.

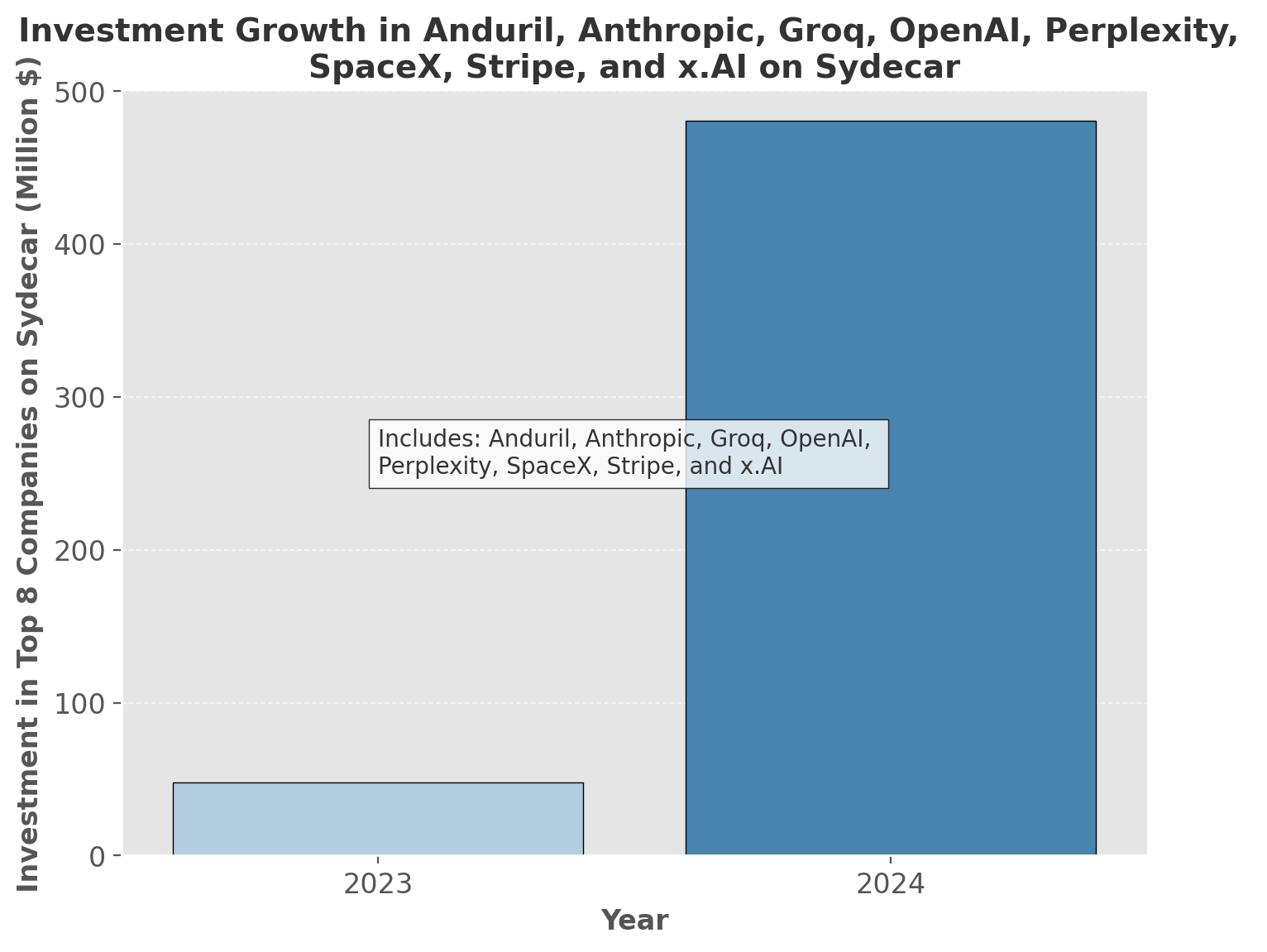

Since January 2024, a staggering 77% of all secondary deals closed on Sydecar have been concentrated in just eight technology leaders: Anduril, Anthropic, Groq, OpenAI, Perplexity, SpaceX, Stripe, and x.AI.

This "Elite Eight" has become a gravitational center for secondary market capital. Collectively, these companies have attracted over $481 million in investment through Sydecar's secondary market infrastructure—representing a 10-fold increase from the $48 million deployed to these same companies in 2023. This isn't merely growth; it's a fundamental reallocation of capital toward perceived category winners.

The concentration is particularly notable given the thousands of venture-backed private companies theoretically available for secondary investment. What we're witnessing is a flight to quality, with investors overwhelmingly focused on companies at the intersection of artificial intelligence and frontier areas like aerospace, robotics and defense tech —sectors perceived to be reshaping the future of the global economy.

There are likely a few reasons for the high investor interest in these specific companies. OpenAI, Anthropic, and other foundation model companies have hit a level of hyper scale never before seen in private startups [e.g. Anthropic went from $0 to about $1 billion in ARR in four years]. Adding fuel is the Trump administration's pro-growth and de-regulatory stance on AI development has created a favorable environment for innovation in these sectors. That along with the heightened geopolitical tensions, described as a "new red Cold War," have shifted the focus to AI as the primary battleground between the U.S. and its adversaries, accelerating spending and innovation. This has also partially led to a dramatic reshuffling of the traditional defense sector hierarchy, with tech first defense companies like Palantir [today at over $200 billion], Anduril, Shield AI and others starting to see meteoric over legacy players like Boeing, a trend which the new US govt. & DOGE is expected to accelerate. A large contributing factor is simply the sheer size of these companies - SpaceX & OpenAI are two of the largest private market companies and as valuation increases, investing volume tends to correlate.

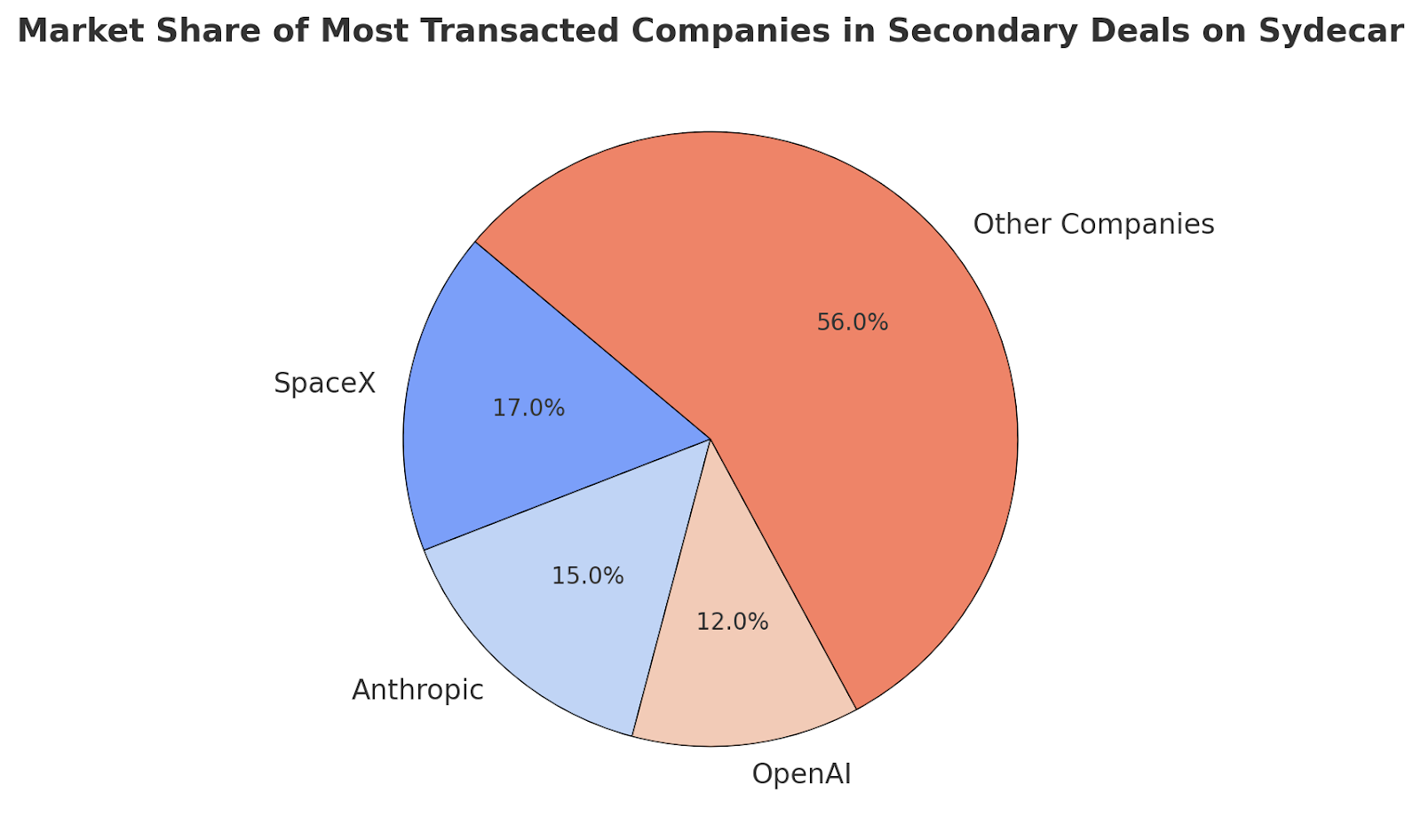

Within this select group, SpaceX leads as the most transacted company, representing 17% of all secondary deals. Anthropic follows closely at 15%, with OpenAI capturing 12% of the market. This concentration illustrates investors' growing appetite for established, high-growth technology companies, particularly those at the forefront of artificial intelligence and space technology. The data overall didn’t shock me though I am a bit surprised to see certain names left out of this cohort like Databricks, Kraken and others.

Nonetheless, the data points to a clear pattern: while the overall secondary market is expanding rapidly, investment dollars are flowing disproportionately toward a relatively small number of premium companies, creating a winner-takes-most dynamic in the SPV ecosystem.

Looking Ahead

Looking ahead to 2025, almost all indicators point toward continued explosive growth in the secondary SPV sector. While some might expect this trend to decelerate as high-profile companies like Stripe, Databricks, and SpaceX potentially go public, historical data suggests otherwise.

When analyzing the aftermath of major tech IPOs from 2020-2023, over 65% of institutional investors redirected portions of their liquidity events back into private market opportunities. Additionally, the convergence of multiple transformative technologies—with AI alone projected to create $15.7 trillion in global economic value by 2030 (PwC)—continues to drive unprecedented institutional interest among retail and institutions. Venture capital funding in frontier technologies (AI, robotics, quantum computing) reached $172 billion in 2023, a 28% increase year-over-year despite the broader market contraction, and there’s little signs of this slowing.

However, there are certainly some very real and concerning trends that could slow secondary investing, mainly that 1) companies are increasingly implementing restrictive transfer policies as they gain leverage in a tightening market, with more sophisticated right of first refusal clauses and outright prohibitions on certain transfers, and 2) legal documentation is already evolving with more explicit anti-syndication provisions in share purchase agreements, preventing buyers from immediately repackaging allocations into SPVs.

Nonetheless, in our view, as these technological revolutions accelerate and institutional appetites for private market exposure grow, secondary markets are positioned to expand regardless of IPO activity. The efficiency, flexibility, and targeting capabilities that SPVs offer will likely cement their role as one of the preferred vehicles for sophisticated investors seeking exposure to market leaders before they reach public markets.

If you enjoyed this article, feel free to view our prior articles on adjacent topics

Last Money in is Powered by Sydecar

Sydecar empowers syndicate leads to manage their investments more effectively. Organize, manage, and engage your investor network effortlessly with Sydecar’s management and communication tools. Their platform also automates banking, compliance, contracts, tax, and reporting, freeing up syndicate leads to focus on securing deals and strengthening investor relations. Elevate your syndicate operations with Sydecar.

If you enjoyed this post, please share on LinkedIn, X (fka Twitter), Meta and elsewhere. It goes a long way to support us!

We’ll be back in your inbox next Wednesday on our next topic. Thanks for tuning in!

Questions? Comments? Feedback? We welcome all, and would love to hear from you!